Valuation & Pricing

How I price a company in 48 hours

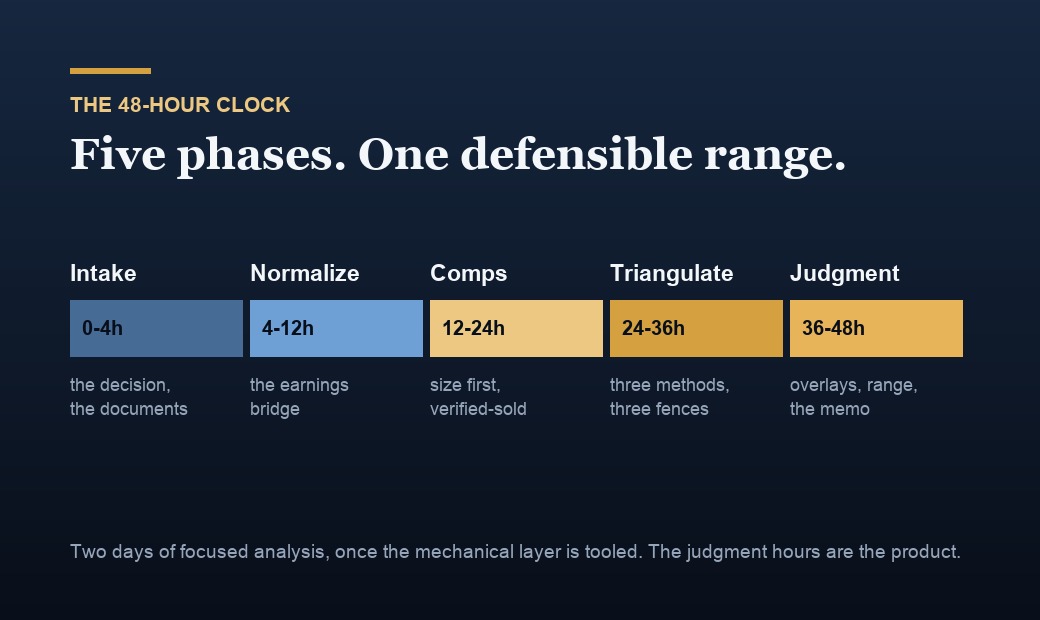

A defensible price is two days of real work, not two months of theater. The full process, hour by hour: intake, normalized numbers, a size-first comp set, triangulation, and a range with every assumption visible.

When you pay someone to value your company, you are not buying a number. You are buying an opinion you can defend. To a buyer. To an investor. To a partner who wants out, or a co-founder who wants in. The number itself is cheap. What costs money is the reasoning that survives contact with the person on the other side of the table.

I have priced more than 1,000 private companies. Before that I spent years in Fortune 500 corporate development, working M&A on deals up to roughly $26 billion, so I spent years being the person on the other side of the table. I founded Value Alpha, a fair-value methodology built with Columbia and NYU faculty. I invest through Sonnerie VC. I did my EMBA at Columbia Business School and I work out of New York. That is the last time I will mention any of it. The rest of this essay is the process. It takes 48 hours. Here is how, and why that is enough.

Why 48 hours is enough

Selling a small business takes about 7 to 9 months on average across most sectors, per the IBBA / M&A Source Market Pulse survey (Q2 2024). Almost none of that time is analysis. It is buyer search, diligence, and negotiation. The pricing work itself, done honestly, is two days of focused effort, if and only if the mechanical layer already exists.

In my own work, roughly 70 percent of a valuation is mechanical: assembling comps, checking normalization math, running sensitivities. That split is my heuristic from a thousand of these, not a market statistic. I built Value Alpha so that layer is tooled rather than hand-cranked, which frees all 48 hours for the 30 percent that is judgment, the only part anyone should be paying for. Productize the inputs. Spend judgment where judgment is scarce.

Two things this is not. It is not a formal appraisal; if you need a number for the IRS or a courtroom, you need a credentialed appraiser and I will tell you so. It is not a fairness opinion. It is a decision-grade pricing opinion: an independent range, delivered while the decision is still live, with every assumption visible.

Hours 0 to 4: intake, and the questions that kill deals early

The first question is not about the company. It is about the decision. Are you selling, buying, marking a position, settling a dispute? The decision determines the standard of value and the buyer lens. As I put it in my Valuation 101 guide, if you do not know which kind of buyer is at the table, strategic or financial, you do not know the price.

Then the document list: three years of financials plus the matching tax returns, revenue by customer by year, what the owner actually does and what the owner is actually paid, key contracts, and an org chart. The clock starts when the documents land.

The intake questions kill weak deals early, which is a service in itself. If revenue by customer does not exist as a report, that tells me something. If the tax returns and the financials disagree, that tells me more.

Hours 4 to 12: normalize before you multiply

Rebuild the earnings before touching any multiple. Owner compensation reset to market. One-time items out. Personal expenses out. Family payroll priced at market or removed. Every adjustment gets a written reason, not just an entry, because every adjustment is a claim a buyer's diligence team will attack.

This is not a private preference of mine. In the Pepperdine Private Capital Markets Report, the recast, meaning adjusted, EBITDA multiple is consistently the most-used method among business appraisers, and it was the top choice again in the 2025 report. The multiple gets the attention. The recasting is where the argument lives.

Then choose the earnings basis deliberately. For an owner-operated company under roughly $5 million, seller's discretionary earnings, SDE, is the honest basis. Above that, adjusted EBITDA. They are not comparable, because EBITDA removes owner compensation and SDE keeps it, so the same business reads differently on each. Mixing them is the most common self-inflicted wound in small-company pricing.

Finally, split the revenue by quality: recurring versus one-time, concentration, retention. The output: a normalized earnings bridge, one line per adjustment, each line defended.

Hours 12 to 24: the comp set, size first

Two rules govern the comp set.

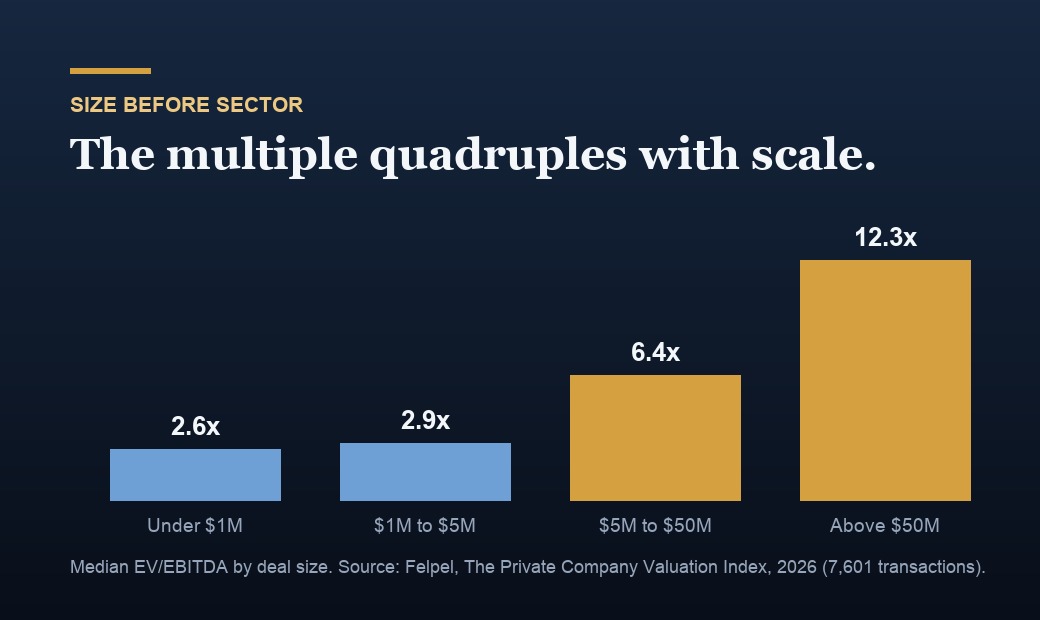

First, size before sector. In my Private Company Valuation Index, built from 7,601 small-business transactions with usable multiples out of a 20,699-deal database, the size effect dwarfs everything else. On an EV/EBITDA basis, deals under $1 million clear around 2.6x, sub-$5 million deals around 2.9x, $5 million to $50 million deals around 6.4x, and deals above $50 million around 12.3x. That is a 124 percent jump just from the sub-$5 million band to the $5 to $50 million band. Sector medians, by contrast, cluster tightly. Scale beats sector, so I band by size first and refine by sector second.

Second, verified-sold over asking. The Index shows active listings asking about 3.26x SDE while verified-sold deals clear about 2.58x. Comp against asks and you inflate the answer before you have done anything else. The overall verified median runs 2.67x SDE, about 7 percent below the 2.86x rule of thumb people carry around.

Each comp that makes the table gets a written reason it belongs and a note on where it differs. The output is a comp table you can argue with, which is the point.

Hours 24 to 36: triangulation, and how each method lies

I run three methods and correct each one for its known lie.

Comparable companies overstate, because a private company is less liquid, more concentrated, and more person-dependent than its comps. Precedent transactions anchor you to deals whose private logic you do not know; maybe that acquirer overpaid for a reason that will never repeat. And a DCF on an early or messy company is your assumptions dressed up as math, so at Main Street scale I treat it as a sanity check, not a driver. For a pre-revenue company the same skeleton runs with financing comps replacing transaction comps, which I cover separately in my pre-revenue pricing essay.

Three methods, three fences. I am not looking for agreement. I am looking for the overlap, and for an explanation of every gap. Triangulation, not an answer.

Hours 36 to 48: judgment, the range, and the memo

This is the part no tool does, and the honest reason is in my own data. Customer concentration, owner dependence, and add-back survival are not in my Valuation Index, because the source records do not capture them. The market data cannot see the things that most often move an individual price. That is not a footnote. That is why these hours exist.

So I go looking for the data-room silences. The question I ask, straight from my Valuation 101 guide: given how this company wants to be seen, what would it least want me to look at? A renewal that is closer and less certain than the narrative implies. An add-back that will not survive diligence. A key employee with no contract and all the client relationships.

Then the buyer-type overlay: who is realistically at the table, and what that does to the range. A strategic buyer with real synergies can rationally pay more than a financial buyer. But as I wrote in what acquirers really pay for, the price still has to survive a room inside the buyer, and structure, meaning earnouts, escrows, and retention, is often a price statement in disguise.

Aswath Damodaran's book Narrative and Numbers makes the general case: a valuation holds up only when the story and the model discipline each other. Hours 36 to 48 are that discipline applied in both directions.

The deliverable is a range, never a point. The number you cannot defend a range around is a number you do not understand. The memo shows the fences each method set, every adjustment with its reason, a sensitivity table, and the short list of facts that would change the answer most. A pricing memo the client can argue with, line by line. If you cannot argue with it, it is marketing.

A worked example, clearly labeled illustrative

Everything below is an illustrative composite, not a client.

Call it Meridian Partners, a professional-services firm. $4.0 million revenue, 14 staff. The owner is the lead rainmaker. About 60 percent of revenue sits on annual contracts. The top client is 22 percent of revenue.

Hours 4 to 12, the bridge, on an SDE basis because the firm is owner-operated and under $5 million:

- Reported pre-tax profit: $610k

- Add back owner salary: +$150k

- Add back depreciation and interest: +$25k

- Add back a one-time legal settlement: +$40k

- Add back personal expenses run through the business: +$35k

- SDE: $860k

Subtract a $160k market-rate replacement manager and adjusted EBITDA is $700k. I state both numbers so the basis discipline stays visible.

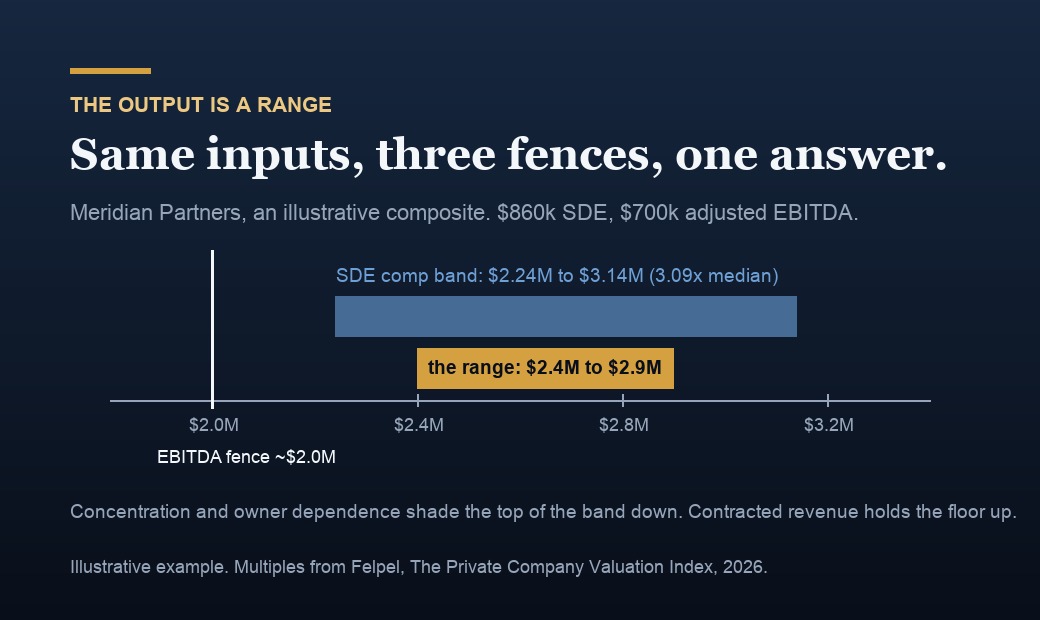

Hours 12 to 24, the anchor: professional and B2B services in my Valuation Index runs a median 3.09x SDE, interquartile 2.60x to 3.65x, on 452 deals. Straight math: $2.24 million to $3.14 million, midpoint near $2.66 million.

Hours 24 to 36, the cross-check: on the EBITDA basis, sub-$5 million deals in the Index cluster near 2.9x, so $700k times roughly 2.9x lands around $2.0 million. That lower fence says the top of the SDE band needs earning, not assuming. A DCF at this maturity is a sanity check, and it stayed one.

Hours 36 to 48, the overlays, each one named:

- 60 percent contracted revenue argues for the top half of the band.

- The 22 percent client shades it down.

- The owner-as-rainmaker problem shades it down further, or pushes value into an earnout, which is a price statement in disguise.

- Net: a defensible range of roughly $2.4 million to $2.9 million.

Two sensitivities make the memo teachable. Every 0.25x of multiple is about $215k of price on this SDE, so multiple arguments are $200k arguments. And at roughly 3x, every dollar of add-back that survives diligence is worth about three dollars of price, while every add-back that dies costs three. That is why the bridge gets built line by line.

One more line the memo says out loud: a listing priced at the 3.26x asking norm from my Index would put this business near $2.8 million and feel validated, while verified-sold data says deals like it clear about 7 percent under the rule of thumb. Both facts go in the memo. That is what independence buys.

Where this sits next to a broker's opinion and a formal appraisal

A broker's opinion of value is usually free, and it is priced to win a listing, so the incentive tilts optimistic. That is structure, not dishonesty. My Index quantifies the outcome market-wide without naming anyone: asks around 3.26x, verified-sold around 2.58x. I carry no success fee and no listing to win. The only deliverable is a number I can defend to the other side of the table.

A formal appraisal is a different tool for a different job. It exists for the IRS, courts, and estates. It follows professional standards, takes weeks, and is worth every one of them when compliance is the job. An appraisal defends a number to a regulator. My memo prices a decision that is live this quarter: the LOI on the desk, the mark, the buyout conversation. When your question is tax or litigation, hire a credentialed appraiser, and I will say so on the first call.

What to demand from any valuation you pay for

Whoever you hire, including me, demand four things.

A range, with the assumptions visible. A written reason for every comp and every adjustment. A named earnings basis, SDE or EBITDA, chosen deliberately and never mixed. And the short list of facts that would change the answer, because a valuation that cannot tell you what would move it is not analysis, it is a horoscope.

If you want the mechanical layer yourself, my valuation calculator and pricing checklist are free, the Valuation Index is published in full, and if your company is AI-native there is a separate benchmark for that. If you want the 48 hours, book a call.

The 48 hours

Need a number you can defend?

If you are selling, buying, marking, or settling and the number matters, I deliver an independent, decision-grade pricing opinion in 48 hours: a defensible range, every assumption visible, built on the Value Alpha methodology and my published transaction data. Tell me the decision on the table.

Common questions

How can 48 hours be enough when selling a business takes the better part of a year?

Because pricing and selling are different jobs. The IBBA / M&A Source Market Pulse survey puts the average small-business sale at about 7 to 9 months, but almost all of that is finding a buyer, diligence, and negotiation. The analysis itself is two days of focused work when the mechanical layer, comps, normalization, sensitivities, is already tooled. I built Value Alpha so the 48 hours go to judgment, not data assembly.

What do you need from me before the clock starts?

Three years of financials and the matching tax returns, revenue by customer by year, what the owner actually does and is paid, key contracts, and an org chart. The clock starts when the documents land. Gaps do not stop the work; they show up as wider bands and explicit assumptions in the memo.

Why do I get a range instead of a single number?

Because a single number hides its assumptions and a range exposes them. The number you cannot defend a range around is a number you do not understand. The memo shows the fences each method sets, the adjustments I made and why, and the two or three facts that would move the answer most.

Do you value on SDE or EBITDA?

It depends on who runs the business day to day. For owner-operated companies, seller's discretionary earnings is the honest basis. For larger firms with a management layer, adjusted EBITDA. They are not interchangeable, since EBITDA removes the owner's compensation, so EBITDA multiples read higher on the same business. The Pepperdine Private Capital Markets Report shows recast EBITDA is the profession's standard basis, and the recasting is where most of the argument lives.

Is this a formal appraisal I can use for the IRS or in court?

No, and it is not trying to be. Tax and litigation need a credentialed, standards-compliant appraisal, and I will tell you when that is the tool you need. This is a decision-grade pricing opinion: an independent, defensible range delivered while the decision is still live, with every assumption visible so you can argue with it.

Related reading

- How to value a pre-revenue startup, from someone who prices them.

- What acquirers really pay for when they buy your company.

- Your 409A is not your valuation.

- How to read a cap table before it reads you.

Tomasz Felpel is an investor, founder, and advisor in private markets and healthcare, based in New York. He is a three-time founder of Value Alpha, an AI-powered private-markets valuation platform, Sonnerie VC, an early-stage healthcare venture firm, and Pond. Previously he led corporate development and M&A at Fortune 500 scale, pricing more than 1,000 private companies. Columbia Business School EMBA. Read the full story.