Corporate Development & M&A

What corporate development really pays for when it buys your company

I sat on the buy side and priced more than a thousand private companies. The acquirer does not pay for what you think, and does not price you the way a VC does. Here is the logic, from the seat across the table.

I spent years on the buy side. Corporate development and M&A at Fortune 500 scale, deals that ran up toward twenty-six billion dollars, and somewhere north of a thousand private companies priced. I want to tell you something that took me years on that side of the table to say plainly. The acquirer does not pay for what you think it pays for, and it does not price you the way a venture capitalist does.

If you ever sell your company, the person on the other side will be running a logic you have probably never seen written down. This essay writes it down. Build for it now, while you still have time to change the answer.

The buyer is not a VC, and that changes everything

A VC prices your future as a standalone bet. They buy a slice, hold it, and pray for a power-law outcome where one winner pays for nine corpses. They are pricing optionality and dilution math. A strategic acquirer is doing the opposite. They are pricing your company inside theirs. They do not care about your standalone trajectory the way your seed investor did. They care about what the combined entity is worth once you are folded into their operations, their distribution, their cost base, and their roadmap.

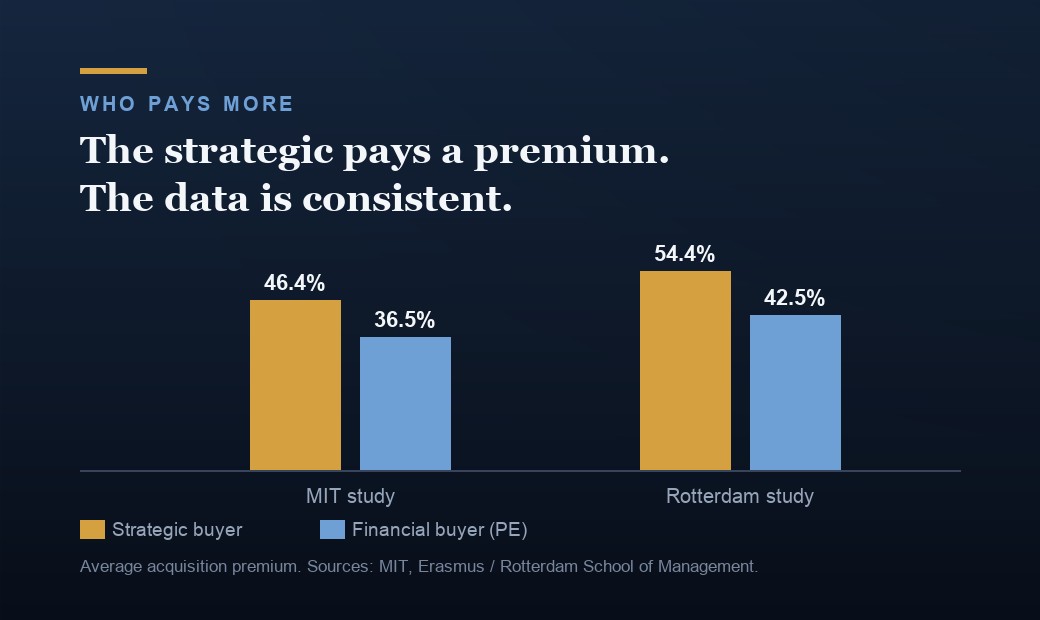

That single shift is why strategics, on average, pay more. Three university studies make the gap concrete. MIT found strategic winners in US deals paid a 46.4% premium over recent trading value versus 36.5% for financial buyers. Copenhagen Business School found 28% versus 22% across Western Europe. Rotterdam found 54.4% versus 42.5%. The strategic pays more because only the strategic can underwrite synergy. The caveat: this is not a law. In recent software M&A, private equity has matched or beaten strategics, roughly 8.9x revenue versus 8.6x in one sample of public deals. Dry powder and add-on platforms can flip it. But the default is that the buyer who can fold you in pays the most, and that buyer is pricing the merger, not the company.

What a strategic actually pays for

Strip away the deck language and there are a handful of real reasons a strategic writes a check. Synergy is the headline, and it splits two ways. Cost synergy: overlapping functions, duplicate vendors, redundant headcount. Revenue synergy: cross-selling you into their installed base, or them into yours. Know the difference, because the buyer does. Cost synergies get captured at roughly 70 to 85% of what gets announced, inside about eighteen months. Revenue synergies land at maybe 25 to 35%, over three to five years, if ever. A buyer who has done this before discounts your revenue story hard and pays mostly for what they can cut.

After synergy comes capability and IP: a technology they would otherwise spend years building. Team: in a pure acqui-hire the price is the people, roughly one to three million per engineer, sometimes five for elite talent, and much of that "price" is actually retention packages routed to employees, not your cap table. AI has detonated this. Big Tech spent over forty billion on acqui-hires and reverse acqui-hires in 2024 and 2025. Microsoft-Inflection at about 650 million, Google-Character.AI near 2.7 billion, Google-Windsurf around 2.4 billion, often structured as a license-and-hire that deliberately leaves the corporate shell behind to dodge merger review. Time-to-market: Cisco built 200-plus acquisitions on one premise, voiced by its old head of business development, that if you are a year late the market may not exist anymore. Defensive value: sometimes the buyer is paying to deny you to a rival. Meta paid 19 billion for WhatsApp partly to keep Google from getting it. And distribution: an installed base and a channel are themselves the synergy.

How the price gets justified inside the building

Here is the part founders never see. Nobody at the acquirer wakes up empowered to hand you a number. The number has to survive a room. A corp-dev person builds a synergy model, runs accretion-dilution math, and writes a memo that an internal champion carries to a deal committee and then a board. Your price is not what you are worth. It is what someone inside the buyer can defend as worth it.

This is where most of the value gets destroyed, and you should understand why so you do not become the cautionary slide. The discipline, if the buyer is any good, follows Damodaran: separate the company as-is from the control value from the synergy value, and never double-count. Control value lives entirely inside your company. Any competent owner could capture it, so a buyer can rationally pay close to all of it. Synergy requires both firms, so they should pay only a fraction. Add a control premium on top of fully-valued synergy and you have paid twice for the same dollar. The honest framing comes from Sirower's Synergy Trap: the premium is not upside, it is a debt the buyer must repay through specific performance gains beyond what both firms were already going to do alone. The premium compounds at the cost of capital while synergies ramp slowly, which is why so many premium deals quietly destroy value.

The evidence is brutal. McKinsey found about a quarter of deals overestimated cost synergies by at least 25%, and nearly 70% missed their revenue-synergy targets. A KPMG study of large deals found 53% destroyed value and only 17% created it. Roughly half of acquisitions are eventually divested. None of this means your buyer is stupid. It means the room they have to convince has seen those numbers too, and they are skeptical of yours.

How corp dev runs the process, and what kills deals in diligence

The process is a funnel designed to find reasons not to pay. The price you hear in the indicative term sheet is the high-water mark. From there, diligence exists to chip it down. The market reaction at announcement, by the way, is predictive: deals where management can present a detailed, credible synergy breakdown sized to the premium tend to be received well and to perform. Conseco's stock fell about 20% on the Green Tree deal. Avis rose about 9% on Zipcar. The buyer's champion needs your story to be the Avis kind.

What kills deals in diligence is rarely the thing founders fear. It is customer concentration you downplayed. Revenue that turns out to be one-time. A key engineer with no retention hooks. Messy cap tables, unassigned IP, a contractor who wrote core code and never signed it over. A churn curve that looks worse under cohort analysis than in your blended number. Every one of these hands the buyer's deal team ammunition to re-trade the price, and a single re-trade can erase more value than months of your selling did.

Why structure beats the headline number

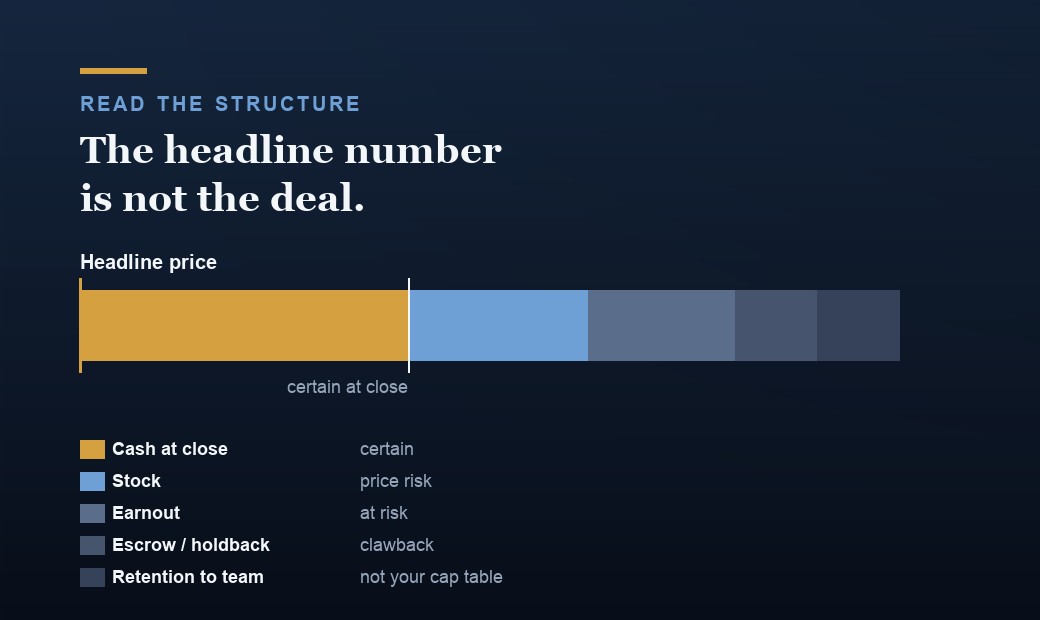

Founders fixate on the headline. Buyers fixate on structure, because structure is where they manage the risk that your synergy story is fiction. Earnouts push a chunk of the price behind milestones you have to hit post-close, often after you have lost control of the levers that hit them. Stock versus cash decides whether you get certainty or a bet on the acquirer. Retention and vesting can route a stunning share of "the price" to employees over four years rather than to the cap table. Escrow and holdbacks park money against reps you made about the business. A 100-million headline with a heavy earnout, a long retention vest, and a fat escrow can be worth far less than an 80-million all-cash deal that closes clean. Read the structure before you celebrate the number.

The founder mistakes that leave money on the table

The biggest one: running a single-bidder process. Prices commonly rise 50 to 100% when a proprietary conversation becomes a competitive one. A buyer talking to you alone is pricing you against their walk-away, not against a rival. Second: pitching your standalone dream instead of their synergy. The founder who shows the buyer exactly which costs combine and which customers cross-sell is handing the champion their board memo. Third: confusing the VC's diversification logic for the strategic's. Diversification adds no value here. Conglomerates trade at a 5 to 10% discount because investors diversify more cheaply than you can for them. Fourth: negotiating price while ignoring structure. Fifth: letting diligence surprise the buyer. Every surprise is a re-trade.

Build so the buyer's logic works in your favor

You cannot control whether you get acquired. You can control whether the buyer's machine produces a high number when you do. Make your synergy obvious and your risk boring. Own your IP cleanly. De-concentrate your revenue. Put retention hooks on the people a buyer would pay millions to keep. Document the cost overlaps and cross-sell paths a champion will need. And never, ever let yourself be the only name on the page.

I priced more than a thousand private companies from the buyer's chair. The ones that got paid the most were not the ones with the best story. They were the ones built so that the logic on my side of the table had no choice but to land on a big number. Build for the seat across from you. It is the only seat that sets your price.

Common questions

Do strategic buyers really pay more than private equity?

On average, yes, and the gap is measurable. Academic studies put strategic premiums roughly 6 to 12 points above financial buyers: MIT found 46.4% versus 36.5%, Rotterdam 54.4% versus 42.5%. The reason is synergy, which only a strategic can fold into existing operations. But it is not a law. In recent software deals, private equity has matched or beaten strategics, around 8.9x revenue versus 8.6x. Dry powder and add-on platforms can flip the rule in specific windows.

What is the difference between cost synergies and revenue synergies, and why does it matter to a founder?

Cost synergies are savings from cutting overlap: duplicate functions, vendors, headcount. Revenue synergies are new sales from cross-selling the combined products. It matters because buyers trust them very differently. Cost synergies get captured at roughly 70 to 85% of the announced figure within about eighteen months. Revenue synergies land at maybe 25 to 35%, over three to five years. A seasoned buyer discounts your revenue story hard and pays mostly for what they can reliably cut. Build your pitch accordingly.

Why does deal structure matter more than the headline price?

Because structure is where the buyer parks the risk that your value story is wrong. A high headline can hide a heavy earnout tied to milestones you no longer control, a four-year retention vest that routes money to employees instead of the cap table, and an escrow held against your reps. An 80-million all-cash deal that closes clean can beat a 100-million deal loaded with contingencies. Read earnouts, stock versus cash, vesting, and holdbacks before you celebrate any number.

What kills an acquisition during diligence?

Usually the unglamorous things. Customer concentration you downplayed. Revenue that turns out to be one-time. A key engineer with no retention hooks. Unassigned IP or a contractor who wrote core code and never signed it over. Churn that looks worse under cohort analysis than in your blended number. Each one hands the buyer's deal team a reason to re-trade the price downward, and a single re-trade can erase more value than months of selling created. Fix these before anyone looks.

How should a founder position the company to maximize the acquisition price?

Make the buyer's logic land on a big number. Run a competitive process, never a single bidder; prices commonly rise 50 to 100% when a sale becomes an auction. Pitch their synergy, not your standalone dream: show exactly which costs combine and which customers cross-sell, so their internal champion can carry it to the board. Own your IP cleanly, de-concentrate revenue, and put retention hooks on the people they would pay millions to keep. Make synergy obvious and risk boring.

Related reading

- How to value a pre-revenue startup, from someone who prices them.

- AI-native valuation: pricing companies built on rented models.

- The valuation index: how I think about private-market pricing.

- Building without warm intros: why the outsider's rigor became my edge.

Go deeper

If you are building toward an exit, or staring at a term sheet you are not sure you read correctly, let's work the actual numbers together, or read more of how I think about it.

Tomasz Felpel is an investor, founder, and advisor in private markets and healthcare, based in New York. He is a three-time founder of Value Alpha, an AI-powered private-markets valuation platform, Sonnerie VC, an early-stage healthcare venture firm, and Pond. Previously he led corporate development and M&A at Fortune 500 scale, working on deals up to roughly $26 billion and pricing more than 1,000 private companies. Columbia Business School EMBA. Read the full story.