Founders · Valuation

Your 409A is not your valuation

Founders carry one number in their head, the post-money from the last round. A private company has at least two prices, and knowing which one answers which question is basic financial literacy.

One number in your head, two prices on your company

I price private companies for a living. I have priced more than a thousand of them and worked on deals up to roughly $26 billion in value, and I can tell you the most common financial literacy gap I see in founders. It is not discounted cash flow. It is not cap table math. It is this: founders carry exactly one number in their head, the post-money from their last round, and they use it to answer every question anyone asks. What is the business worth? Post-money. What are my engineer's options worth? Post-money divided by shares. What should an acquirer pay? Post-money plus a premium. That number is the wrong answer to almost every one of those questions.

It is also usually old. In Q2 2024, per Carta's own data, the median startup raising a Series A on its platform had waited 774 days since its previous primary round. The number in your head is often more than two years stale before you replace it.

Here is the fact underneath this entire essay: a private company has at least two prices at all times. There is the negotiated price investors paid for preferred stock, a security loaded with liquidation preferences and rights. And there is the appraised fair market value of plain common stock, the paper you and your employees actually hold. Both numbers are correct at the same moment. They answer different questions. Knowing which price answers which question is basic financial literacy for a founder, and almost nobody teaches it.

What a 409A actually is, and why the safe harbor matters

Section 409A is a tax statute, not a valuation philosophy. It entered the Internal Revenue Code through the American Jobs Creation Act of 2004, signed into law on October 22, 2004, and it exists because of Enron, where executives accelerated deferred compensation and exercised options at inflated valuations while the company collapsed underneath them. Congress responded by taxing deferred compensation that plays games with value. Stock options are the startup version of the problem: under the Treasury regulations, an option granted with a strike price below the fair market value of the underlying stock is treated as nonqualified deferred compensation and falls inside 409A. An option granted at or above fair market value is exempt.

The penalty structure is what should get your attention, because it does not land on the company. It lands on your employees. On a failure, the vested deferred compensation becomes immediately includible in the employee's gross income, plus an additional federal tax of 20 percent, plus interest at the IRS underpayment rate plus one percentage point. California stacked its own 20 percent on top until AB 1173 cut the state add-on to 5 percent in 2013; before that, a California employee could face a combined 40 percent in additional taxes before ordinary income tax and interest even entered the math. Grant options carelessly and you are not risking your money. You are risking theirs.

The regulations offer a way out, and it is the reason the 409A industry exists. Fair market value for private stock must come from the reasonable application of a reasonable valuation method, and the rules bless three safe harbor approaches. The one nearly everyone uses is an independent appraisal, dated no more than 12 months before the grant. The prize is a shifted burden of proof: with a safe harbor valuation in hand, the IRS cannot simply disagree with your number. It must prove that your method, or how you applied it, was grossly unreasonable. That is a high wall, and per Carta's guide it costs roughly $1,000 to $10,000 from a traditional firm. Cheap insurance. But be clear about what you bought: a tax compliance appraisal of common stock whose main job is setting the minimum strike price for employee options. Not a scoreboard.

What a 409A values, and why common is worth less than preferred

Your Series A investor did not buy the stock you hold. Preferred stock carries a liquidation preference, so in a bad exit the preferred gets paid before common sees a dollar, and it usually carries anti-dilution protection, board seats, and blocking rights on top. Common stock is a minority position with none of that and no market to sell into. So when an appraiser values common after a priced round, the standard tool is the option pricing model backsolve: it assumes the new investors paid fair value for their preferred, then allocates the company's equity value across share classes using Black-Scholes, with breakpoints set by the liquidation preferences, as a16z's explainer on the method lays out. On top of the allocation comes a discount for lack of marketability, typically 25 to 35 percent for a two-year expected holding period, per a16z.

The output surprises founders every single time, so look at the market-wide data first. Per Carta platform data shared by Peter Walker of Carta Insights in April 2024, common stock fair market value sits at a 77.3 percent discount to the most recent preferred price at seed, 71.7 percent at Series A, 65.8 percent at Series B, and 60.8 percent by Series D. In plain terms: when a seed investor pays $1.00 for preferred, the common is worth about 22 cents. That is not a scandal. That is the price of the preference stack plus illiquidity, calculated.

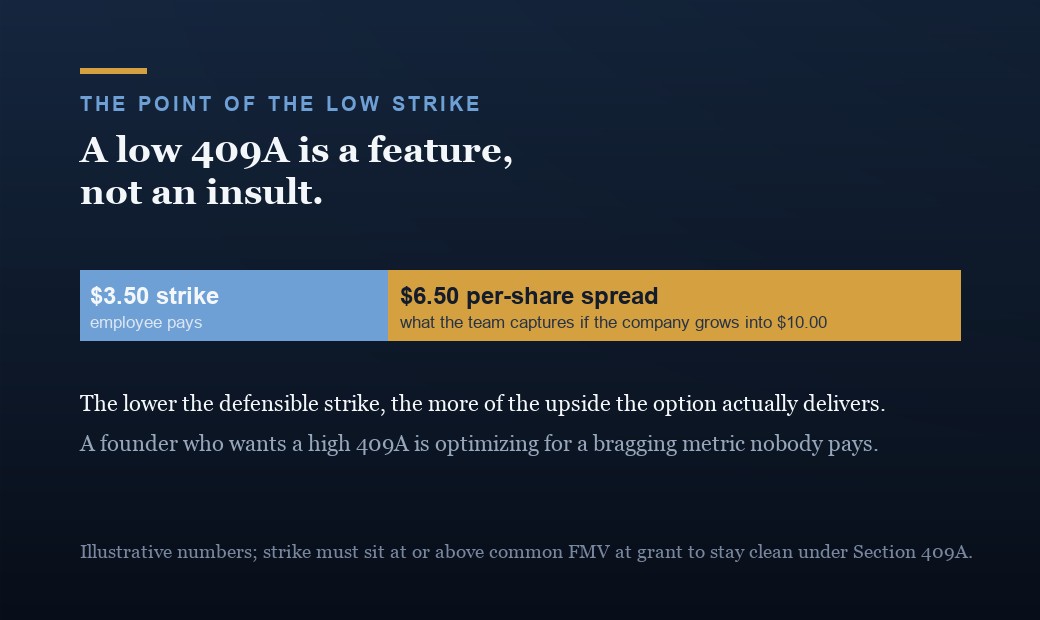

Make it concrete with an illustrative example. Your Series A prices preferred at $10.00 per share, post-money $40 million. Weeks later, the board approves a 409A appraisal valuing common at $3.50 per share, 35 percent of the preferred price. Same company. Same day. Two correct numbers. The $10.00 answers one question: what does a new investor pay for preferred stock wrapped in preferences and rights? The $3.50 answers a different one: what is a single share of illiquid common worth today, to a minority holder standing behind the preference stack? Neither number is wrong. They are correct answers to two different questions.

A low 409A is a feature, not an insult

Founders read the $3.50 as a slap. Our own appraiser thinks we are worth a third of what investors just paid? That is the wrong reading. Follow the employee's money instead. An engineer granted options at a $3.50 strike, in a company whose preferred just priced at $10.00, holds the right to buy in at roughly a third of what sophisticated investors paid. If the company simply grows into its preferred price, she captures the spread. That spread is the entire point of an option, and a low, defensible 409A is the mechanism that makes startup equity worth taking. The operative word is defensible. Carta's guide flags 'the lower the strike price, the better' as a myth for exactly this reason: an artificially low strike is a red flag for auditors and the IRS, and if the strike is found to be below fair market value, the immediate income tax, the 20 percent additional tax, and the interest all land on your employees. The goal is the lowest defensible price.

Two more myths, both dead. First, the old rule of thumb that a 409A should simply be 10 to 20 percent of the preferred price: Carta and a16z both reject it, because value must be allocated across share classes based on actual preferences, participation, and conversion rights, not a lazy fraction. Second, the idea that the discount is permanent. It shrinks every round in Carta's data, from 77.3 percent at seed to 60.8 percent at Series D, for a mechanical reason: preferred converts into common at IPO, so the two prices are forced to converge as a listing approaches. The SEC polices the endgame, reviewing option grants made in the 12 to 18 months before an IPO; a significant gap between strike prices and the IPO price triggers the cheap stock problem and unfavorable accounting treatment, per a16z.

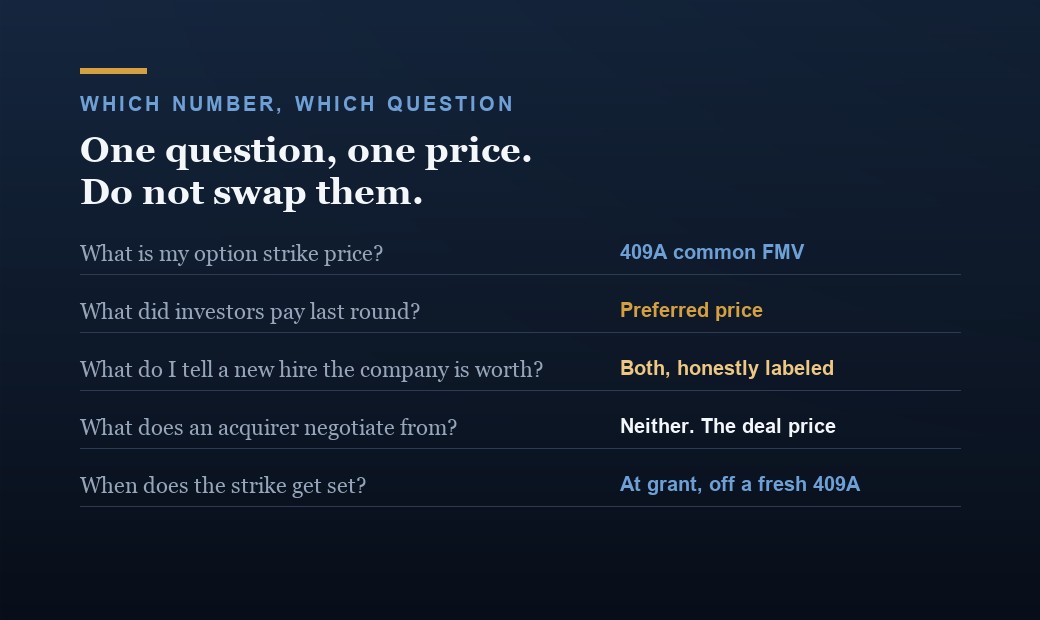

Which number answers which question

Employees. The 409A sets the strike, and the honest recruiting pitch is the spread. Tell a candidate: you buy in at $3.50, investors just paid $10.00, and the gap narrows as we move toward an exit. Do not tell them the company is worth $40 million and let them multiply their ownership by it. At seed, common is worth about 22 cents on the preferred dollar per Carta's data, so post-money math overstates their equity several times over.

Investors. They set the preferred price by negotiation, and they do not care what your 409A says as a price. They care that your option granting is clean, because they are buying into your cap table and inheriting its problems.

Acquirers. Neither number is the answer. An acquirer prices the whole business through its own diligence, and both your post-money and your 409A are historical data points. But your 409A hygiene matters enormously here: acquirers scrutinize 409A practices in M&A diligence, and sloppy ones can shift tax liability to the buyer or force indemnification, per a16z. A clean appraisal history is worth real money at exit.

Banks and lenders. They lend against cash flow, collateral, and covenants. Quote your post-money to a credit officer and watch their face do exactly nothing. A valuation is only meaningful with the question attached, and their question is whether you can service debt.

Secondaries deserve their own line, because founders fear them for the wrong reason. A sale of common covering less than roughly 10 percent of fully diluted shares generally has little to no impact on the 409A, per Eqvista. For company-run tender offers, Carta reports the 409A will likely rise, but often not meaningfully if controls are in place, such as limiting who may participate. And tender pricing tracks the primary market: in 2024, 60 percent of tender offers priced exactly at the last preferred round, per Carta, with any discount reflecting that tendered shares are common while investors bought preferred.

The mistakes that cost the most

Letting the 409A go stale. A safe harbor valuation lives for a maximum of 12 months, or until a material event, whichever comes first. Material events include closing any new financing, whether a priced round, a SAFE, or a convertible note, receiving a credible acquisition term sheet, and major changes in projections or business model, per Carta. Grant options on a stale valuation and the safe harbor evaporates, which means the burden of proof lands back on you.

Quoting post-money to employees. Covered above, but it bears repeating because it is the mistake that costs trust rather than money. When employees discover the gap on their own, and they always do, you have taught them to discount everything you say about their equity.

Negotiating M&A off the 409A. The appraisal deliberately prices a minority, non-marketable slice of common stock. It is a floor for tax purposes, not an anchor for a control transaction where a buyer takes the whole company. Founders who internalize the 409A as the real number negotiate against themselves.

Ignoring repricing after a down market. This is the freshest scar. In Q1 2023, 23 percent of 409A valuations delivered on Carta declined from their prior value, nearly four times the share from Q1 2021, and 45 percent of Series D valuations fell, per Carta's 2023 trends report. The same report shows Series D pre-money valuations dropping by more than half from Q1 2022. When the new 409A lands below existing strikes, options go underwater, and Carta's data shows employees are far less likely to exercise underwater options, especially departing employees who typically have only 90 days to decide. The fix is repricing: in 2023, 873 companies on Carta repriced nearly 100,000 option grants, increases of 33 and 39 percent year over year, per Carta's compensation report. Repricing is board-level work, administratively messy, with tax implications for the changed grants. Pretending your team's equity still works is messier.

The takeaway

Carry both numbers, and attach the question to each. The post-money is what an investor paid for a preferred slice of your future, wrapped in protections you do not get. The 409A is what your common stock is worth today: appraised, defensible, deliberately conservative, and legally load-bearing for every option you grant. One number recruits capital. The other protects your team from the IRS. The gap between them is not embarrassing, it is the priced cost of preferences and illiquidity, and it closes on schedule as you march toward an exit.

You do not have a valuation. You have valuations, plural. The founders I trust with big numbers are the ones who know which one to quote.

Common questions

How often does a company need a new 409A valuation?

A safe harbor 409A is valid for a maximum of 12 months from its effective date, or until a material event occurs, whichever comes first, per Carta's guide. Material events include closing any new financing, whether a priced round, a SAFE, or a convertible note, receiving a credible acquisition term sheet, major changes in financial projections, and strategic partnerships that change the business model. In practice you need a 409A before issuing your first stock options, after every material event, and at least every 12 months. Granting options on an expired valuation forfeits the safe harbor protection.

Why is a 409A so much lower than the post-money valuation?

Because the two numbers price different securities. The post-money reflects what investors paid for preferred stock, which carries liquidation preferences and other rights. A 409A appraises common stock, a minority and illiquid position behind the preference stack, and applies a discount for lack of marketability that a16z pegs at 25 to 35 percent for a two-year holding period. Per Carta data shared by Peter Walker in April 2024, common carries a 77.3 percent discount to the preferred price at seed, narrowing to 60.8 percent by Series D. The gap is priced structure, not pessimism.

What happens if options are granted below fair market value?

The consequences land on the employee, not the company. Under Section 409A, the option becomes nonqualified deferred compensation: vested amounts are included in the employee's income immediately, plus an additional 20 percent federal tax, plus interest at the IRS underpayment rate plus one percentage point. California adds its own 5 percent penalty, reduced from 20 percent by AB 1173 in 2013. This is why an artificially low strike is not a perk. The goal is the lowest defensible price under a safe harbor appraisal, which forces the IRS to prove the valuation was grossly unreasonable.

Will a secondary sale or tender offer spike our 409A?

Usually less than founders fear. Secondary transactions involving less than roughly 10 percent of fully diluted shares generally have little to no impact on the 409A, per Eqvista, and the fewer shares involved, the smaller the effect. For company-run tender offers, Carta reports the 409A will likely rise, but often not meaningfully if proper controls are in place, such as limiting the number of permitted participants. Tender pricing itself tracks the primary market: in 2024, 60 percent of tender offers priced exactly at the most recent preferred round, per Carta, because tendered shares are common while investors bought preferred.

Who can perform a 409A valuation and what does it cost?

For the independent appraisal safe harbor, a qualified independent third party must produce a written report using generally accepted valuation methods, per Carta's guide. The separate illiquid-startup presumption is where the regulations' experience test lives: it requires a valuation by someone with significant knowledge and at least five years of relevant experience in valuation, financial accounting, investment banking, or comparable fields. A standalone 409A from a traditional firm costs roughly $1,000 to over $10,000 depending on company size and complexity. Once delivered, the board should formally approve the new fair market value, and every new option grant must be priced at or above that number.

Related reading

- Raising on SAFEs: the dilution you signed and forgot.

- How to read a cap table.

- How to handle a down round when the terms matter more than the price.

- How to value a pre-revenue startup, from someone who prices them.

Go deeper

If you are about to grant options or walk into a raise with one number in your head, let's get both numbers right together before the next grant or term sheet, or read more of how I think about it.

Tomasz Felpel is an investor, founder, and advisor in private markets and healthcare, based in New York. He is a three-time founder of Value Alpha, an AI-powered private-markets valuation platform, Sonnerie VC, an early-stage healthcare venture firm, and Pond. Previously he led corporate development and M&A at Fortune 500 scale, pricing more than 1,000 private companies. Columbia Business School EMBA. Read the full story.