Building & Career

How to read a cap table before it reads you

A valuation operator who prices private companies for a living on the three things a cap table actually tells you, and why the ownership column is the least useful of them.

I price private companies for a living. I have priced more than a thousand of them and worked on deals up to roughly $26 billion, and the cap table is the document founders are most likely to nod along to and least likely to actually read. They open it, find the row with their name, read the percentage next to it, and close the file. That percentage is the one number on the page that tells you the least. A cap table is not a list of who owns what. It is a forecast of who gets paid what, and when. Read it that way and it stops being an accounting artifact and becomes the most honest document in your company. Let me show you how to read it the way the investor across the table already does.

Start with what the thing is. A capitalization table is the ledger of every claim on the company: common shares, preferred shares, the option pool, warrants, and the SAFEs and convertible notes that have not turned into shares yet but will. Each row carries not just a count but a set of terms, and the terms are where the document earns its keep. The count tells you ownership today. The terms tell you what that ownership is worth on the day it matters. Most founders read the counts and ignore the terms, which is exactly backwards.

The layers: every cap table is a stack of claims

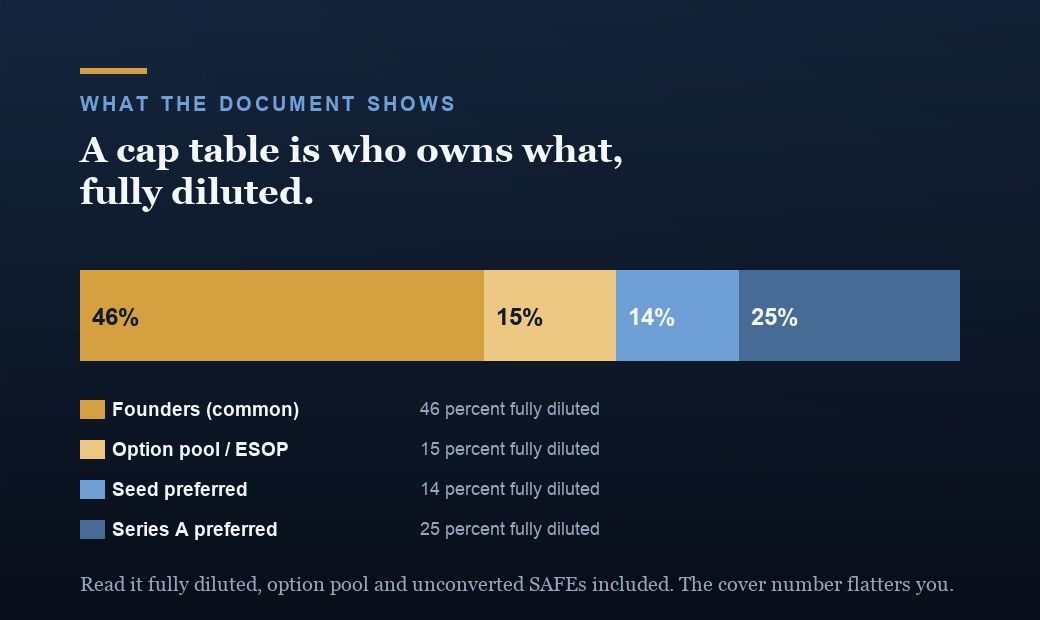

Picture a company a couple of rounds in. The cap table has settled into layers. At the bottom sits common stock, held by founders and, through exercised options, employees. Above it sits the option pool, the reserved equity set aside to hire and retain. Above that sit the preferred layers, one per priced round, Seed then Series A, each with its own price, its own preference, and its own protections. A clean way to see it: founders and common might hold something like 46 percent, the option pool 15 percent, Seed preferred 14 percent, and Series A preferred 25 percent. The exact split is particular to each company, but the shape is universal. You are always the bottom layer, and every layer above you has rights you do not.

Why does the stacking matter before we touch a single number? Because the order is the whole game. Seniority decides who gets paid first in a sale and whose vote can block a financing. When you read a cap table, do not read it as a pie. Read it as a stack, from the top down, because that is the order in which money comes out of it.

The denominator: issued versus fully diluted

Here is the first place founders get the number wrong, and it is almost always wrong in their favor, which is why they like it. There are two ways to count the shares, and they give you two different ownership percentages. Issued shares count only the stock that has actually been granted. Fully diluted shares count everything that can become a share: the entire option pool, including the part that has not been handed out yet, every outstanding warrant, and every SAFE and convertible note sitting on the table waiting to convert. Your real ownership is your shares over the fully diluted total, and it is always the smaller, less flattering figure.

The gap between the two is not small, and it is not academic. The unallocated option pool alone can be 10 to 20 percent of the company, and a stack of uncapped or low-cap SAFEs from a busy pre-seed can convert into far more ownership than the founder remembers agreeing to. If anyone quotes you a percentage without saying the words fully diluted, recompute it yourself. I have watched founders celebrate holding a majority on an issued basis and discover they were already a minority once the pool and the notes were counted. The fully diluted number is the only one an investor uses, so it is the only one you should use too.

Dilution: your slice shrinks every round

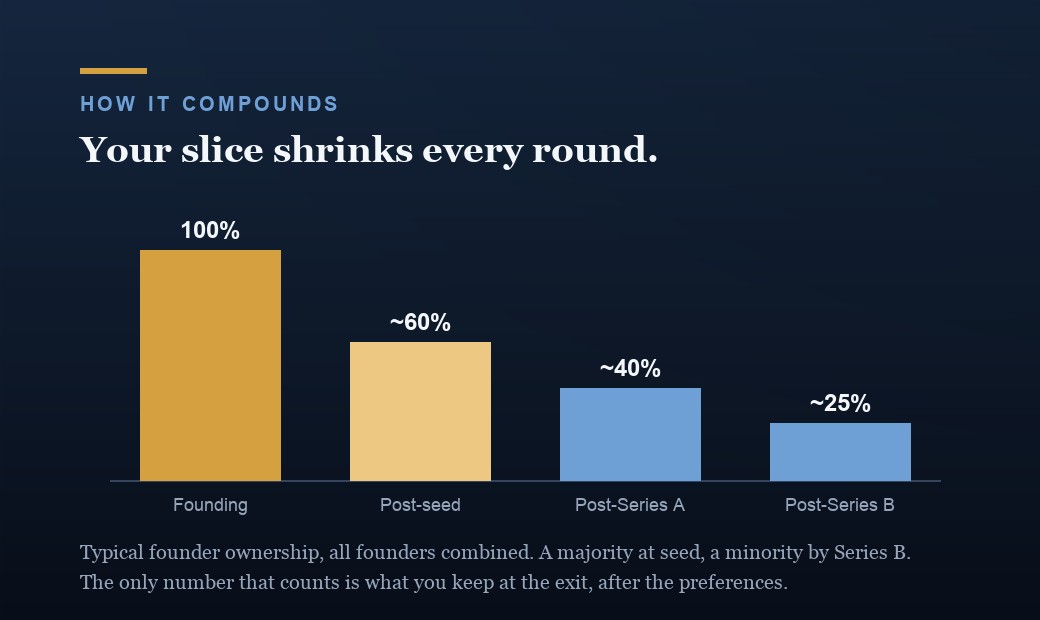

Now watch the cap table move through time, because it is not a snapshot, it is a trajectory. Every priced round issues new shares, and new shares mean your percentage falls even though your share count does not change. This is dilution, and it is not a bug. It is the price of capital, and it is supposed to happen. The founder who raises four rounds and ends with a smaller percentage of a far more valuable company has done the math right. The mistake is not being diluted. The mistake is not knowing by how much, or letting it happen through terms instead of through price.

A common arc looks like this: founders start at 100 percent, sit around 60 percent after a seed round, near 40 percent after Series A, and around a quarter after Series B. Yours will differ, but the direction never does. Two things make the slope steeper than it needs to be, and both hide in the terms rather than the price. The first is the pre-money option pool, which I will come to in a moment. The second is anti-dilution, the provision that reprices earlier preferred at the expense of common if you ever raise at a lower price. Read both before you sign, because they decide how much of the dilution lands on you specifically rather than getting shared across everyone.

The option pool: the dilution that is only yours

The option pool deserves its own paragraph because it is the most common place founders give away ownership without noticing. Investors almost always require the pool to be created or expanded pre-money, meaning before their check is added to the cap table. A pre-money pool is carved out of the existing shareholders, so founders and prior holders absorb 100 percent of it and the incoming investor absorbs none. That is the option-pool shuffle, and it quietly lifts the investor's effective ownership for the exact same price per share. A pool sized by convention rather than to a real plan is pure giveaway. Size it to an honest 12-to-18-month hiring plan, put that plan in writing, and negotiate the pool as part of the price. A point or two of pool moved from pre-money to post-money is worth more to you than most of what you will argue about on the valuation itself.

The waterfall: ownership is not payout

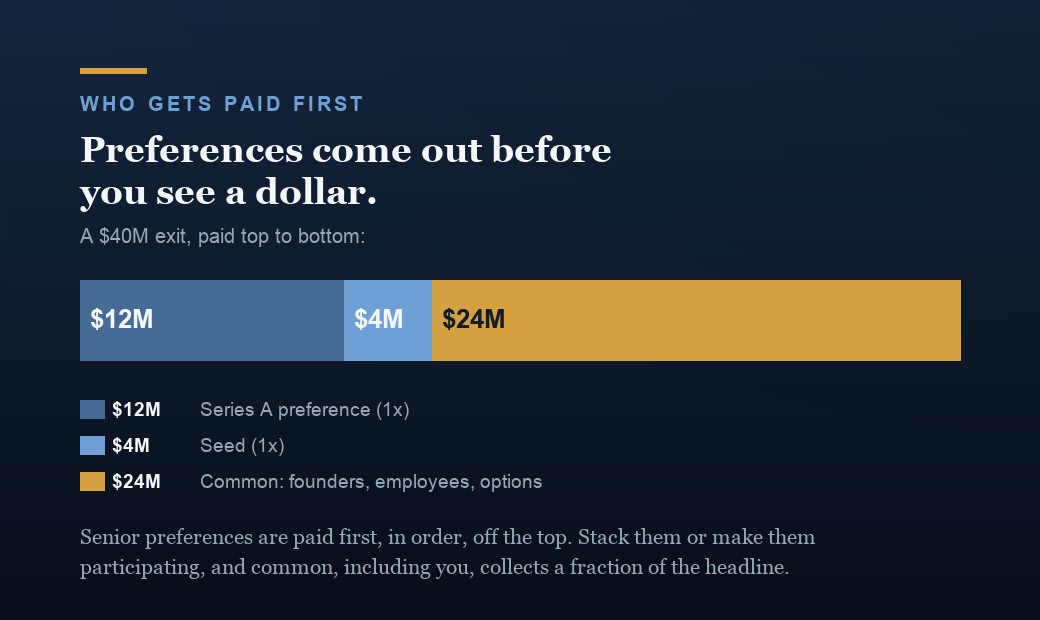

This is the part of the cap table that ownership percentage hides completely, and it is the part that decides what you take home. When a company is sold, the proceeds do not get split by ownership. They get split by the liquidation waterfall, and the waterfall pays the preferred stack first. Each preferred round usually carries at least a 1x preference, meaning it gets its money back, in order of seniority, before common sees a dollar. Only what is left after the entire stack is satisfied gets divided among common by ownership. Owning 20 percent of the company does not mean 20 percent of the sale. It means 20 percent of whatever is left after the preferences are paid.

Walk a clean example. A company sells for $40 million, with $12 million of Series A and $4 million of Seed ahead of common, each carrying a 1x preference. Those preferences come off the top first, $16 million in total, and the remaining $24 million flows down to common. The detail that decides the rest is whether each preference is participating. With nonparticipating preferred, the gentle version, an investor takes the greater of its preference or what it would receive by converting to common, so on a strong exit it simply converts and rides its ownership. With participating preferred, the painful version, it takes the preference and then also shares in the remainder as if it had converted, double-dipping on the way out. Stack a couple of 2x participating preferences and a modest exit can leave common with almost nothing, even at a headline price that sounds like a win. The ownership column will not warn you about any of this. The waterfall will, and it is the only number that tells you what your equity is actually worth.

So when you read a cap table, do not stop at the percentages. Read the preference multiple on every preferred row, read whether each one is participating or nonparticipating, and read the seniority order. Then model the waterfall at a few exit values, a modest one, a base case, and a strong one. The same stake can be worth almost nothing on a soft exit and close to its full percentage on a strong one, and the only way to see which world you are in is to run the math at several prices.

The lines founders miss

A few rows do quiet damage and rarely get read. SAFEs and convertible notes are a shadow cap table: they do not show up as shares until they convert, so a founder can read a clean-looking table that is about to absorb a wave of conversion at the next priced round. A post-money SAFE at least makes the math knowable on day one, since ownership sold equals the investment over the post-money cap, so $1 million on a $6.7 million cap is about 15 percent. The catch is that the cap is post all the other SAFE money only, so the priced round and its fresh pool still dilute it, and that 15 percent can land closer to 9 percent once the Series A closes. Add every SAFE and note up on an as-converted basis before you trust any percentage. Dead equity, stock held by a departed co-founder or an inactive early advisor, is worse than it looks, because it cannot do any more work yet it still dilutes everyone and absorbs its share of every future round. Anything past roughly 10 percent sitting dead is a flag, especially if it exceeds what an active founder still holds. Pro-rata rights let existing investors keep their percentage by buying into future rounds, which is fine until a large early holder's pro-rata crowds out the room you needed for a new lead. And warrants, often attached to venture debt, are real dilution hiding in a financing you booked as non-dilutive. None of these sit in the ownership column. All of them change what the ownership column means.

How to actually read one

Here is the order I read a cap table in, and it is almost the reverse of how founders read it. First, the preference stack: total it up, note every multiple, flag anything participating or above 1x, and read the seniority. That tells me how much of any exit is spoken for before common. Second, the fully diluted denominator: the whole pool, every SAFE and note as-converted, every warrant, so I am working with the real total and not the flattering one. Third, the waterfall, modeled at several exit values, because that is the only thing that converts all of the above into what each holder actually receives. Only then, fourth, do I look at the ownership percentages, which now mean something because I know what sits on top of them. The headline percentage is the last thing I read, not the first.

The takeaway from someone who prices them

A cap table is a structure problem disguised as a spreadsheet. The number founders fixate on, their ownership percentage, is the output of everything else on the page: the denominator that counts it, the dilution that erodes it, and the preferences that decide what it pays. Read those three first and the percentage finally tells the truth. Read the percentage alone and you are reading the one cell on the page designed to make you feel better than your actual position warrants. Ownership is the headline. Dilution and the waterfall are the story. Learn to read the story, and you will negotiate the terms that matter instead of the number that does not, and you will know exactly what you own long before the day it gets tested.

Common questions

What is a cap table and what does it actually tell you?

A capitalization table is the ledger of who owns what in a company: every share, option, warrant, SAFE, and convertible note, and the terms attached to each. Read literally, it tells you ownership percentages. Read properly, it tells you two more important things: how much each holder's slice will shrink as the company raises more money, and who gets paid in what order when the company is sold. Ownership percentage is the headline. Dilution and the payout waterfall are what the document is actually for.

Issued shares versus fully diluted shares: which number matters?

Fully diluted, almost always. Issued shares count only stock that has actually been granted. Fully diluted counts everything that can become a share: the entire option pool including the unallocated part, outstanding warrants, and every SAFE and convertible note that will convert at the next priced round. Your real ownership is your shares divided by the fully diluted total, and it is always a smaller number than the issued figure suggests. If someone quotes you a percentage without saying fully diluted, assume it is flattering and recompute it yourself.

Does owning 20 percent of a company mean I get 20 percent of the exit?

No. Ownership percentage is what you get only after the liquidation preferences are paid. Preferred investors are paid first, in order of seniority, usually at least the money they put in. Only the cash left after that stack is split by ownership. On a modest exit the preferences can absorb most or all of the proceeds, so a meaningful common stake can be worth far less than the percentage implies, and on a strong exit the same stake pays close to its percentage. The only document that tells you the truth is the exit waterfall, not the ownership column.

Why does expanding the option pool dilute founders and not the new investor?

Because investors almost always require the pool to be created or topped up pre-money, meaning before their investment is added to the cap table. A pre-money pool is carved out of the existing shareholders' ownership, so founders and prior holders absorb all of it and the incoming investor is diluted by none of it. This is the option-pool shuffle, and it quietly raises the investor's effective ownership for the same price. Size the pool to an honest 12-to-18-month hiring plan and negotiate it as part of the price, not as an afterthought.

What is the first thing to check on a cap table before signing a term sheet?

The preference stack and the fully diluted math, together. Add up every liquidation preference and its multiple to see how much comes off the top before common sees a dollar, then model the exit waterfall at a few exit values to see what your stake is actually worth. At the same time, recompute your ownership on a fully diluted basis including the unallocated pool and every SAFE and note. Most founders read the valuation and the ownership percentage and stop there. The preferences and the fully diluted denominator are where the real position lives.

Related reading

- How to handle a down round when the terms matter more than the price.

- How to value a pre-revenue startup, from someone who prices them.

- What acquirers really pay for when they buy your company.

- The cofounder is the most expensive line on your cap table.

Go deeper

If you are staring at a cap table or a term sheet and you are not sure what you actually own, let's model the fully diluted math and the exit waterfall together before you sign, or read more of how I think about it.

Tomasz Felpel is an investor, founder, and advisor in private markets and healthcare, based in New York. He is a three-time founder of Value Alpha, an AI-powered private-markets valuation platform, Sonnerie VC, an early-stage healthcare venture firm, and Pond. Previously he led corporate development and M&A at Fortune 500 scale, pricing more than 1,000 private companies. Columbia Business School EMBA. Read the full story.