Building & Career

How to handle a down round when the terms matter more than the price

A valuation operator who reads cap tables for a living on why the headline number is the least important part of a down round, and how the structure and the dilution math decide what actually happens to you.

I price private companies for a living. I have priced more than a thousand of them and worked on deals up to roughly $26 billion, and the most common thing I see founders get wrong about a down round is which number they are watching. They watch the headline valuation. They obsess over whether the post-money has a lower digit in front of it than last time. The headline valuation is the least important number in a down round. The terms decide what happens. The dilution math decides what it costs. The headline is just the press release. I read cap tables, and I price the consequences of a financing, so let me tell you where the money actually moves.

Start with what a down round even is. It is a priced round at a lower price per share than your last priced round. That is the whole definition. It is not a moral judgment, and right now it is not even rare. They peaked in the 2023 to 2024 cycle: Carta's data put the down-round share at roughly 19 to 20 percent of all priced rounds every quarter of 2023, and on a like-for-like basis Cooley's own client financings hit an all-time high of 32 percent of deals in the first quarter of 2024. The market has since healed. Carta had it under 14 percent by the end of 2025, the lowest in three years, and Cooley's repriced-deal rate fell to 12.8 percent. So if you are staring at one now, you are not a special case of failure. You are a normal case of a market that overpriced your last round.

Why the headline is a distraction

Here is why I keep saying the headline does not matter. Two down rounds can print the identical lower valuation and do completely opposite things to your ownership and your future. One can leave your cap table clean and your team motivated. The other can quietly hand a third of your company to your existing preferred holders, stack liquidation preferences on top of your common, and force every employee underwater. Same headline. Different planet. The price tells you almost nothing. The structure tells you everything, and the structure is where sophisticated investors do their work while founders argue about the valuation.

So stop negotiating the headline first. Negotiate the structure first, then the price. A founder who understands this has leverage. A founder who does not is the one who signs a flat round to protect their ego and discovers a year later that the terms underneath it cost them more than a clean reset ever would have.

The real cost: where the money actually moves

The down round itself dilutes you, because new shares get issued at a lower price, so you sell more of the company for the same dollars. That part is obvious. The expensive part is what the down round triggers. Anti-dilution provisions reprice your prior preferred at the direct expense of common, which means at your expense and your employees' expense. Almost every priced round your investors did already carries anti-dilution. The only question is which kind, and the two kinds are not close.

Walk the math with me, because this is the single most important paragraph for a founder facing a reset. Say founders hold 2,000,000 common shares and your Series A bought 1,000,000 shares at $10.00, a $10 million round, so there are 3,000,000 shares total and you own 66.7 percent. Now you raise a down round at $6.00 per share. Under full ratchet, the worst form, the Series A conversion price resets all the way down to $6.00, and their 1,000,000 shares become about 1,666,667. That is 666,667 extra shares handed to your investor for free, and it cuts you from 66.7 percent to about 54.5 percent before the new money even lands. Under broad-based weighted average, the standard form, the conversion price only resets to $8.40, which gives the investor roughly 190,000 extra shares. Same down round, same price, and full ratchet hands the investor about 476,000 more shares than weighted average does. That gap is the cost of one word in a term sheet you signed years ago.

The good news is that broad-based weighted average is the overwhelming market standard, the standard in venture deals, while a full ratchet is now rare. If your old term sheet has weighted average, the anti-dilution hit is survivable. If a new investor tries to slip full ratchet into the down round itself, understand exactly what they are charging you and price it against the alternatives below.

Then there is the dilution that arrives before a single new dollar does. The option-pool shuffle: when a new investor requires you to expand the option pool pre-money, that fresh pool is carved out of the pre-money cap table, so existing holders, meaning you, absorb 100 percent of it. The incoming investor is not diluted by it at all. That structure quietly adds several points to investor effective ownership, and a pool sized to convention instead of to an honest 12-to-18-month hiring plan makes a down round strictly worse, because you are taking that hit at the lower price. Top-ups between rounds are the most expensive way to fund a hire, because they dilute you with zero new capital coming in.

Two more line items founders miss. Dead equity makes a down round structurally worse, because stock held by departed co-founders or inactive advisors cannot absorb its share of the new dilution as sweat, so active founders and the option pool eat more of the round. The common red line is roughly 10 percent of the company sitting dead, especially if it exceeds what an active founder still owns. And option repricing is the predictable aftershock: a lower 409A pushes employee grants underwater, so you reprice to keep people. Carta saw startups reprice just under 100,000 option grants across 2023 as the downturn bit. Repricing is not free, though. To stay clean under Section 409A the new strike has to sit at or above current fair market value, and it triggers fresh stock-comp expense. The morale and signaling cost is real too, but it is downstream of the structure. Fix the structure and the signaling mostly takes care of itself.

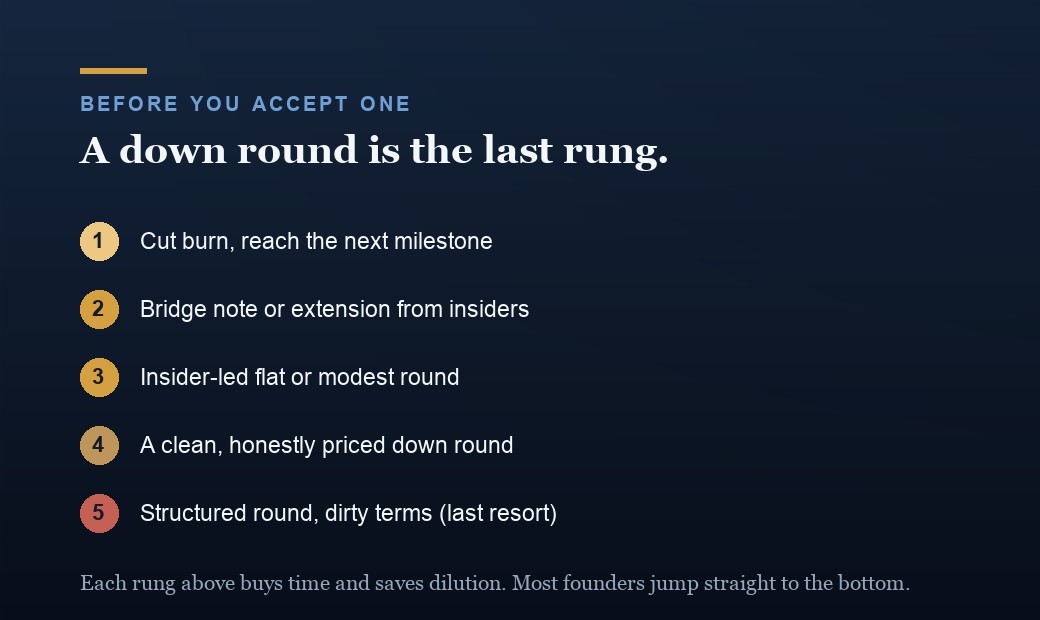

The alternatives founders skip

Before you price a down round, price the things that let you avoid one, because most founders skip straight to the raise. The first lever is cut burn to a milestone. A down round is often just a timing problem: you ran out of runway one milestone short of the number that would clear a flat or up round. Sometimes the cheapest financing is a smaller team and four more months. Model what one more proof point does to your next price before you sell shares to buy that time.

The second is a bridge or extension, usually a convertible note or a SAFE from your existing investors, to reach that milestone without setting a new price at all. A bridge defers the pricing question, which is exactly what you want when you believe the milestone will move the number. The third is an insider flat round, where your current investors reprice at the prior valuation to keep the cap table clean. None of these is free, and a bridge with a punishing discount or cap can be worse than a clean reset. But a founder who has not modeled all three before taking a structured down round has not actually run the trade.

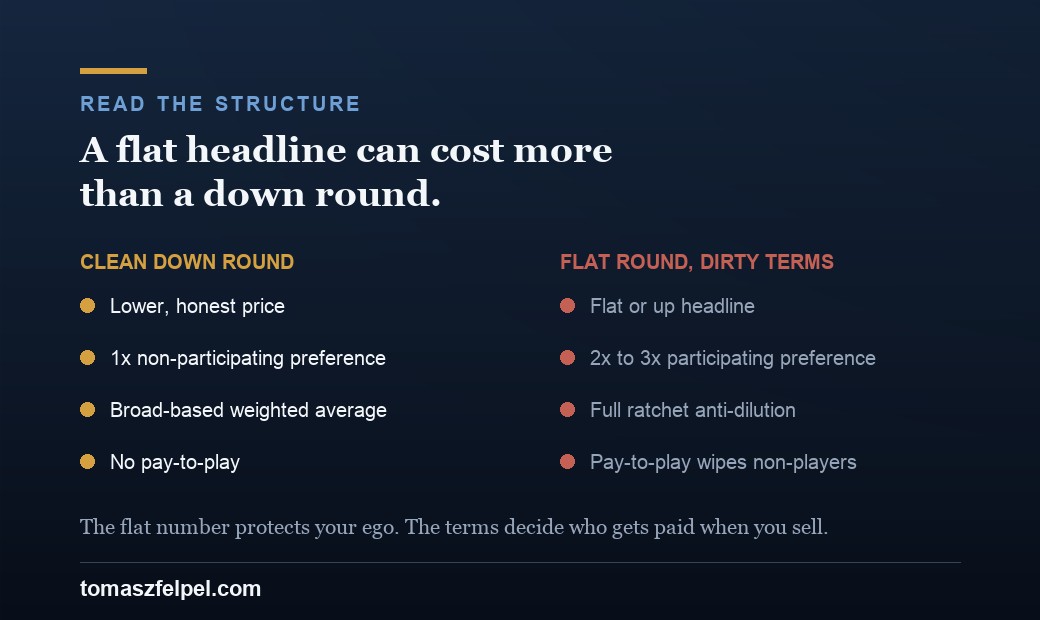

When a clean down beats a toxic flat

This is the trade founders get backwards more than any other. A flat headline feels like a win, so they accept toxic structure to protect it. A clean lower-priced round almost always beats a flat round dressed in multiple liquidation preferences, full-ratchet anti-dilution, and pay-to-play. Run the waterfall, not the headline. A 2x or 3x participating preference stacked to hold a flat number means the investors get their money back two or three times over before common sees a dollar, so on most realistic exits your flat valuation is worth less to you than a lower clean price would have been. A flat round with senior stacked preferences is a down round wearing a costume, and the costume costs extra.

Today's market context helps you here. Even as down rounds rose, terms stayed largely company-favorable: Cooley's late-2025 data shows 98 percent of deals with a 1x liquidation preference and 96 percent nonparticipating. So if an investor is pushing a 2x participating preference or full ratchet to hold a flat price, they are reaching well past market, and you should treat the toxic term as the real price of that headline. Take the honest lower number, keep 1x nonparticipating, and keep your waterfall clean.

How to actually run it

Run the cap table and the waterfall before you run the process, not after. Model the post-round cap table and the exit waterfall at three or four exit values for every structure on the table, so you can see exactly what each term does to common at a modest exit, a base-case exit, and a home run. The headline valuation will not show you that. The waterfall will, and it is the only document that tells you which deal is actually better for the people building the company.

Handle your existing investors as the partners with the most to lose, because they are. Use that. Pay-to-play, where investors who do not participate in the down round lose preferences or convert to common, is a legitimate tool to pull your insiders into the round and clean up the ones who will not support you. Bring the board the waterfall, not the press release, and frame the choice as common-value-preserving, because that aligns founders, employees, and the long-term investors against the short-term-optimizing ones. Then protect employee equity deliberately: plan the repricing or option refresh as part of the round, not as a panicked afterthought three months later, and communicate it before rumor does it for you.

The mistakes that cost the most

Delay is the most expensive mistake. Founders burn six months chasing a flat round that is not there, spend down their runway, and arrive at the down round weaker, with less leverage and worse terms than if they had moved when they had three quarters of cash left. The price you are avoiding gets worse the longer you avoid it. Chasing the headline is the second: trading clean structure for a flat number, which is how you end up with the toxic costume above. Ignoring the structure is the third, signing a term sheet on price alone and discovering the anti-dilution, the preference stack, and the pre-money pool only after they have done their damage. And neglecting the team is the fourth, letting underwater options and silence do the work that a planned reprice and a straight conversation should have done. Each of these is avoidable, and each one is more expensive than the down round itself.

The takeaway from someone who reads the cap table

A down round is a math and structure problem, not an emotional one. I have watched it from both sides of the table, as the operator pricing the consequences and as the investor sitting across from the founder, and the founders who come out fine are never the ones who fought hardest for the headline. They are the ones who negotiated the terms first, modeled the waterfall before they signed, worked the cheaper alternatives before they reset the price, and chose a clean lower number over a flat number wearing toxic structure. The valuation is the part everyone talks about. The terms and the dilution math are the part that actually decides what you keep. Watch the right number, and a down round is just a reset. Watch the wrong one, and it is the most expensive thing you will ever sign.

Common questions

What actually costs the most in a down round, the lower valuation or the terms?

The terms, almost always. A lower price dilutes you in a predictable way. The structure underneath it is where the real money moves: full-ratchet anti-dilution can hand an investor hundreds of thousands of free shares, stacked liquidation preferences can mean common sees nothing on a modest exit, and a pre-money option-pool expansion dilutes only you. Negotiate the structure first, then the price. The headline is the part everyone watches and the part that matters least.

Is a flat round always better than a down round?

No, and assuming so is how founders get trapped. A flat headline propped up by a 2x participating preference, full ratchet, or pay-to-play is a down round wearing a costume, and on most realistic exits it pays common less than a clean lower-priced round would. Run the waterfall at several exit values, not the headline. Take the honest lower number with 1x nonparticipating preferred and weighted-average anti-dilution over a flat number with toxic structure.

Full ratchet versus weighted average anti-dilution: how big is the difference?

Large. On an identical down round from $10.00 to $6.00 per share, full ratchet resets the prior conversion price all the way to $6.00 and can cut founders from 66.7 percent to about 54.5 percent before new money lands. Broad-based weighted average resets only to $8.40 on the same facts. Full ratchet hands the investor roughly 476,000 more free shares for the same round. Weighted average is the standard in venture deals. Full ratchet is now rare, for good reason.

What should I try before agreeing to a down round?

Work the ladder first. Cut burn to reach the next milestone, since a down round is often just a timing problem one proof point short of a better price. Raise a bridge or extension from existing investors to defer pricing entirely. Ask insiders for a flat insider round to keep the cap table clean. None is free, and a punishing bridge can beat nothing, but a founder who has not modeled all three before taking structured terms has not actually run the trade.

What is the single most expensive mistake founders make on a down round?

Delay. Founders burn months chasing a flat round that is not there, spend down their runway, and arrive at the down round with less cash, less leverage, and worse terms than if they had moved when they had three quarters of runway left. The price you are avoiding gets worse the longer you avoid it. Move early, negotiate the structure, model the waterfall, and protect employee equity before rumor does the talking for you.

Related reading

- How to value a pre-revenue startup, from someone who prices them.

- How to know you have product-market fit, read like an investor.

- What acquirers really pay for when they buy your company.

- The cofounder is the most expensive line on your cap table.

Go deeper

If you are facing a reset, or staring at a term sheet you are not sure you priced right, let's model the cap table and the waterfall together before you sign, or read more of how I think about it.

Tomasz Felpel is an investor, founder, and advisor in private markets and healthcare, based in New York. He is a three-time founder of Value Alpha, an AI-powered private-markets valuation platform, Sonnerie VC, an early-stage healthcare venture firm, and Pond. Previously he led corporate development and M&A at Fortune 500 scale, pricing more than 1,000 private companies. Columbia Business School EMBA. Read the full story.