Founders · Fundraising

Raising on SAFEs: the dilution you signed and forgot

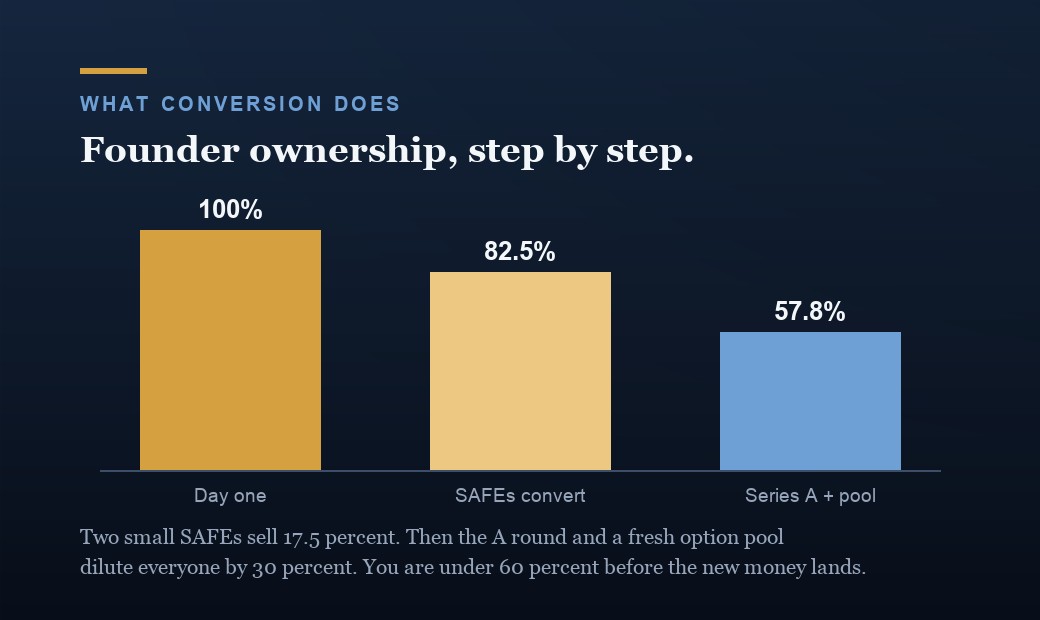

Two small SAFEs eighteen months apart put a founder under 60 percent before the Series A money lands. The math is division. The failure is never doing it.

The five easiest pages in venture finance

I price private companies for a living. I have priced more than a thousand of them and worked on deals up to roughly $26 billion, and I can tell you which documents cause the most founder pain. Not the long ones. The short ones. The NVCA model documents for a priced venture round run past 200 pages and the Series Seed forms run about 38, while a SAFE carries roughly five pages of substantive terms, a contrast the law firm Pillar Legal laid out in its 2023 analysis of the instrument. Five pages feels harmless. Founders sign them between meetings, the wire hits, everyone moves on. Nobody updates the ownership math. That is the trap.

Start with what the thing actually is. The SAFE, Simple Agreement for Future Equity, was introduced by Y Combinator in late 2013 as a replacement for convertible notes, which were then the standard early-stage instrument. It is not debt. It has no maturity date and no interest rate. It converts automatically in any priced preferred round: no minimum raise triggers it, the holder has no say in the matter, and once it converts, the SAFE terminates. Until that round happens, it simply sits on your company. In theory, forever.

And it is everywhere. According to Carta's State of Pre-Seed 2025 in Review, US startups on Carta raised $10.4 billion across 50,316 SAFEs and convertible notes in 2025, and Carta's Q1 2025 data showed SAFEs hitting a record 90 percent of all pre-seed rounds on the platform. Carta calls the post-money SAFE with a valuation cap and no discount the standard pre-seed instrument, with median caps around $10 million for rounds of $250k to $1 million. You will probably raise on SAFEs. Fine. The only question that matters is whether you can state, today, exactly what you have sold.

How a post-money SAFE actually converts

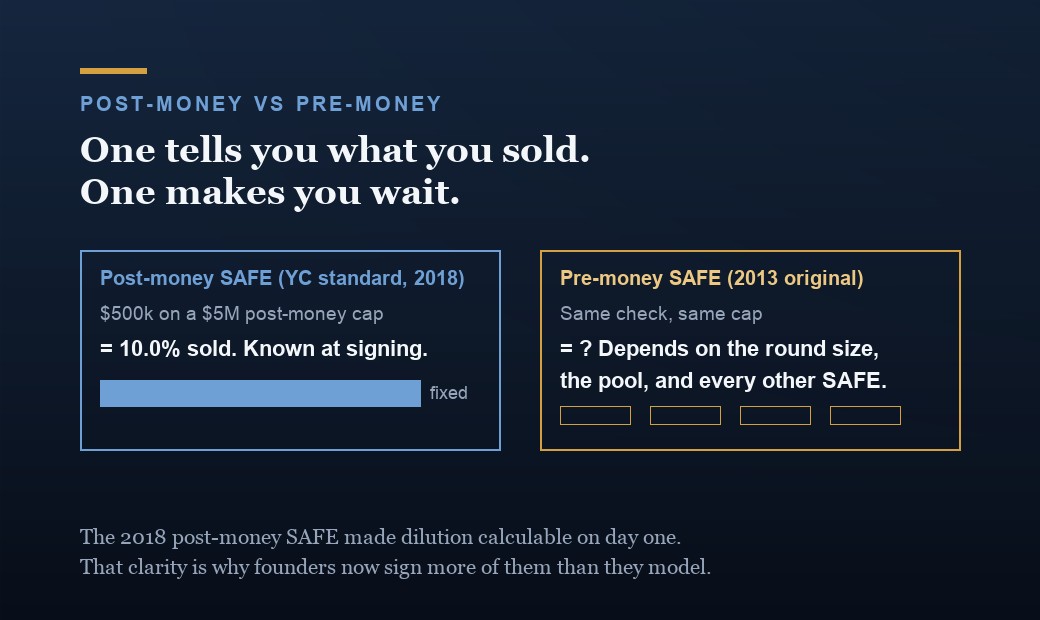

The version you are signing today is almost certainly the post-money SAFE, which YC released in 2018, more than four years after the original. YC's stated reason for the redesign: companies had stopped using SAFEs as short bridges to a priced round and started treating them as independent seed rounds funding multi-year runways. Under the original pre-money form, nobody could answer the simplest question in the deal, how much of the company is being sold, because the answer depended on how much got raised on other SAFEs and on an option pool that would be negotiated years later. YC's own worked example showed a $500k check at a $4.5 million pre-money cap landing anywhere from roughly 7 to 9 percent. An instrument that cannot answer that question is not simple. It is vague.

The post-money SAFE fixed the vagueness with one clean rule: ownership sold equals investment divided by the post-money valuation cap. YC's quick-start examples make the point, raise $500k at a $6.7 million post-money cap and you sold about 7.5 percent, raise $1 million on the same cap and you sold about 15. Under the hood, the conversion price is the cap divided by the Company Capitalization, and the share count is the purchase amount divided by that price. But you do not need the machinery. Division tells you what you sold the moment you sign. Which means there is no longer any excuse for not knowing.

Run it on a stack I see constantly. SAFE 1: $500,000 at a $5,000,000 post-money cap. That sells 10.0 percent. Not roughly, not depending on the pool: 10.0 percent by construction. Eighteen months later the company is further along, so SAFE 2 comes in at a higher cap: $750,000 at a $10,000,000 post-money cap. That sells another 7.5 percent. Post-money SAFEs are not diluted by each other, so the percentages simply add. Before any priced round exists, this founder has sold 17.5 percent of the company. When I ask founders in that seat what they have sold, the usual guess is around twelve. The gap between the guess and the number is not a rounding error. On a company that eventually exits for real money, it is the most expensive five percent they will ever misplace.

The stack problem: dilution accumulates silently

Now the Series A arrives, and here is the part the five pages do not print in bold. The post-money cap is post all the SAFE money, but it is not post the Series A money, and it is not post the new option pool negotiated as part of that round. YC's user guide states both points directly. So when a new investor takes 20 percent and the round adds a 10 percent option pool, everyone on the pre-round cap table is diluted by 30 percent. The founders go from 82.5 percent to about 57.8. The SAFE holders' 17.5 percent becomes about 12.3. The founder who signed two small SAFEs eighteen months apart wakes up under 60 percent of the company before the Series A money even lands. Nothing went wrong. Nobody was greedy. Every line item was standard. The dilution was signed in pieces and never summed.

There is a second asymmetry inside the stack that most founders never read. A post-money SAFE fixes its holder's percentage against every other SAFE and convertible note issued before the priced round. Fixed for them means variable for you. Pillar Legal's 2023 analysis spells out the consequence: until an equity financing happens, the holders of common stock, which in an early-stage company means the founders, absorb the entirety of the dilution from every additional SAFE round. Under the old pre-money form, SAFE holders and founders shared that dilution. Under the current standard form, each new SAFE you sign comes exclusively out of your side of the table.

None of this is a secret. Fred Wilson of Union Square Ventures wrote in 2019 that notes and SAFEs "obfuscate the amount of dilution the founder(s) is taking," described stacks of them collapsing on founders when the priced round finally happens, and recounted talking angry angel investors off the ledge when they saw the cap table and owned far less than they thought. He had made the structural point in 2017: the incoming lead prices its ownership target first, and the notes convert after the founders take that dilution. YC's own quick-start guide contains a worked example in which SAFEs, option grants, and a Series A stack up to 52.62 percent total dilution. And Carta reports 2025 median dilution on SAFE rounds of roughly 19 to 20 percent for rounds between $1 million and $2.4 million, with many deals above 25. The data is public. The arithmetic is division. The failure is behavioral.

Cap, discount, MFN: the terms that set the price

The valuation cap is the term founders anchor on, and it is the term they misread. A cap is a ceiling on the investor's conversion price, not a floor on your valuation. YC's guide is explicit that caps are not final valuations: if your priced round comes in below or close to the cap, the SAFE converts at the round's lower price and takes more ownership than the cap implied. Founders model the cap as the price and stop thinking. Investors model the cap as the worst case and keep thinking. Price the downside before you sign, because the document already did.

Discounts are the quieter lever. Cooley's founder guidance puts typical SAFE discounts between 10 and 25 percent: at a $1.00 Series A share price, a 20 percent discount converts the SAFE at $0.80. When a SAFE carries both a cap and a discount, the investor converts at whichever term gives them the better price, never both, a point Cooley makes plainly. Carta data shared by its insights team indicates that in 2024 roughly 61 percent of SAFEs were cap only and 30 percent were cap plus discount, with the discount almost always set at 20 percent.

The MFN SAFE punts on terms entirely: if a later SAFE gets a lower cap or a bigger discount, the MFN holder can elect those same terms. YC's own standard deal uses one, $125,000 on a post-money SAFE for 7 percent plus $375,000 on an uncapped SAFE with an MFN provision. Pro rata side letters add a further layer, enough that YC publishes a formula for the extra dilution they create. One genuinely founder-friendly mechanic hides in the conversion: SAFE holders receive shadow preferred with a liquidation preference equal to their purchase amount. One times the money, not a multiple of it.

When to stop stacking and price the round

The market already tells you where the line sits. Carta's data from late 2023 through late 2024 shows about 64 percent of seed rounds were SAFEs, and 86 percent of seed rounds under $500k. But above $5 million, only 20 percent were SAFEs and 70 percent were priced equity. Sophisticated money prices real rounds. Meanwhile, per Carta's 2025 pre-seed review, the majority of rounds under $4 million still closed on SAFEs or notes, with founders raising larger and larger sums on convertible paper before switching. That drift is exactly how the stacks in this essay get built.

My rules are simpler than the market's. Price the round when the summed ownership across your SAFEs approaches 20 percent, because from there every additional check compounds a problem instead of funding one. Price it when a single raise runs into the millions. And price it when an investor starts asking for board seats, veto rights, or information rights, because YC's own guide concedes that once ownership certainty is solved, the case for a priced round reduces to exactly those rights. Wilson claimed back in 2017 that a simple priced seed could be done for under $5,000 in a few days. That is his number and it is old, but the direction stands: legal cost stopped being the excuse years ago.

To be fair to the instrument, the SAFE's advantages are real. YC built it for rolling closes, a single negotiated term, no maturity dates to extend, and almost nothing in transaction costs. Those are speed advantages. Use them for speed. The SAFE was never designed to substitute for knowing your own cap table, and it does not become one because signing it felt easy.

The mistakes that cost the most

First, no pro-forma cap table. YC's user guide strongly recommends keeping an accurate cap table that records how each SAFE will convert. Wilson's fix is the same: make your lawyers maintain a pro-forma table showing conversion at different round prices. I see companies raise seven figures without one. The table takes an afternoon. Its absence costs points of the company.

Second, treating the cap as your valuation. It is the investor's ceiling, not your floor, and in a soft round it converts against you. Third, adding checks without adding percentages. Every post-money SAFE is a fixed sale, and fixed sales sum. If you cannot state your running total from memory, you have already lost track of it.

Fourth, signing side letters casually. Pro rata rights look like a courtesy and compound into real dilution at the A, which is why YC hands you a formula for it. Fifth, ignoring the Company Capitalization definition. The entire difference between the pre-money and post-money forms lives in that denominator, and practitioners have published modified language, an approach credited to the lawyer Jose Ancer, that excludes future convertibles so founders and SAFE holders share later dilution instead of founders eating all of it. Ask for it. Sixth, forgetting the downside mechanics. In an acquisition, the SAFE holder takes the greater of their money back or the as-converted value, junior to all debt. In a dissolution they are owed the purchase amount, and there is usually nothing left to pay it. And if you never raise a priced round at all, Cooley notes the SAFE simply never converts. No maturity date means it can outlast your patience.

The takeaway

The SAFE is an honest document. It runs five pages, it hides nothing, and under the post-money form the core question answers itself with one division: money in over cap equals company sold. The dilution that wrecks founders is not smuggled in. It is signed in pieces by people who never keep the running total, then delivered all at once when the priced round converts the stack and layers a new investor and a fresh option pool on top. Every SAFE is a sale of your company at a price you chose under pressure and forgot under momentum. So keep the ledger. Sum the percentages. Model the A round before you sign the next five pages, not after. I read cap tables for a living, and the saddest ones are not the ones where founders sold too much. They are the ones where founders found out.

Common questions

How much ownership does a post-money SAFE actually sell?

Divide the investment by the post-money valuation cap. That is the whole formula. $500,000 at a $5 million post-money cap sells 10 percent; $750,000 at a $10 million cap sells 7.5 percent. Y Combinator's own quick-start guide runs the same math: $500k at a $6.7 million cap is about 7.5 percent. That percentage is fixed against other SAFEs and convertible notes, but not against the priced round: the new investor's stake and any new option pool negotiated in that round dilute SAFE holders along with everyone else.

Do SAFEs dilute each other, or only the founders?

Post-money SAFEs do not dilute each other. Each one locks its holder's percentage against every other SAFE and convertible note issued before the priced round. The mirror image is that founders, as the common stockholders, absorb the entirety of the dilution from each additional SAFE until an equity financing happens, a consequence Pillar Legal's 2023 analysis of the form highlights. Under the older pre-money SAFE, founders and SAFE holders shared that dilution. If you plan to stack several rounds of SAFEs, understand that under the current standard form, every new check comes exclusively out of your ownership.

What happens to a SAFE if we never raise a priced round?

It never converts. A SAFE has no maturity date and no interest rate, and it terminates only on an equity financing, a liquidity event, or a dissolution. If the company is acquired, the holder receives the greater of their money back or the as-converted value at the cap, junior to creditors and any outstanding debt. If the company shuts down, the holder is owed the purchase amount, though as Cooley's guidance notes, meaningful assets rarely remain at that point. If none of those events ever occur, the SAFE simply sits on the company indefinitely.

My SAFE has both a valuation cap and a discount. Which one applies at conversion?

Whichever gives the investor the better price, never both. That is standard, and Cooley's founder guidance states it directly. Typical discounts run 10 to 25 percent: at a $1.00 Series A share price, a 20 percent discount converts at $0.80, and the investor takes that only if the cap-based price is not already lower. In practice the cap does most of the work: Carta data shared by its insights team indicates roughly 61 percent of 2024 SAFEs were cap only, and when a discount appears it is almost always 20 percent. Model both terms before signing, because the investor's counsel already has.

When should I stop raising on SAFEs and do a priced round?

Three triggers. When total ownership sold across your SAFEs approaches 20 percent. When a single raise runs into the millions: Carta's data shows that above $5 million, 70 percent of seed rounds are priced equity and only 20 percent are SAFEs. And when an investor asks for board seats, veto rights, or information rights, since YC's own guide says the SAFE versus priced round question reduces to those rights once ownership certainty is solved. A priced round costs more time and legal fees, but it forces the one thing a SAFE stack never does: a cap table everyone has actually read.

Related reading

- How to read a cap table, from someone who prices them for a living.

- How to handle a down round when the terms matter more than the price.

- How to value a pre-revenue startup, from someone who prices them.

- The cofounder is the most expensive line on your cap table.

Go deeper

If you are sitting on a stack of SAFEs and cannot state your running total, let's model the stack and its conversion at the next priced round together before the next signature, or read more of how I think about it.

Tomasz Felpel is an investor, founder, and advisor in private markets and healthcare, based in New York. He is a three-time founder of Value Alpha, an AI-powered private-markets valuation platform, Sonnerie VC, an early-stage healthcare venture firm, and Pond. Previously he led corporate development and M&A at Fortune 500 scale, pricing more than 1,000 private companies. Columbia Business School EMBA. Read the full story.