Founders · Fundraising

How much should you actually raise?

Founders size rounds by what sounds impressive. The right number works backward from the milestone, the dilution budget, and the bar the money sets. The ask is a valuation decision in disguise.

The ask is a valuation decision in disguise

I price private companies for a living. I have priced more than a thousand of them, worked on deals up to roughly $26 billion, and I invest at the earliest stage through Sonnerie VC, which means I sit on both sides of the same question: how much should this company raise? Founders almost never answer it with math. They answer it with a vibe. A competitor raised $5 million, so $5 million. An investor offered $8 million, so $8 million. The announcement would look thin below $4 million, so $4 million.

Here is what the vibe misses. The amount you raise is a valuation decision in disguise. Every round has two numbers, the check and the ownership it buys, and the market keeps the second one in a fairly narrow band. If investors expect to own 15 to 20 percent and you ask for $6 million, you did not just pick a round size. You claimed a $30 million to $40 million post-money valuation, whether or not your traction supports it, and you signed your next eighteen months up to defend that price. The ask sets the price. The price sets the bar. Most founders pick the ask first and meet the bar later.

This essay is the working-backward version: milestone first, dilution budget second, round size last.

What the runway advice actually says

Ask any investor how much to raise and you will hear the word runway. The canonical sources are more precise than the folklore. Y Combinator's seed fundraising guide, written by Geoff Ralston, says the goal is to raise as much money as you need to reach your next fundable milestone, which will usually be 12 to 18 months out. Fred Wilson published the same arithmetic from the investor's chair on AVC in 2011: for seed, Series A, and Series B, he considers 10 to 20 percent dilution and 12 to 18 months of cash ideal. Paul Graham's formula in How to Raise Money is the bluntest of the three: multiply the number of people you want to hire by $15,000 by 18 months. The $15,000 is deliberately high, meant to cover salary, benefits, office space, and a margin of error. YC's guide carries the same rule of thumb for an engineer, the most common early hire, at about $15,000 a month all-in.

Notice what none of them say. None of them say 24 months. The now-common advice to raise two years of cash is market practice born of a slower market, not canon, and I will show you below where the extra months legitimately come from. Notice the more important thing too: runway is measured in months but denominated in milestones. Eighteen months of cash that runs out short of a fundable milestone is not runway. It is a countdown.

The dilution budget comes first

Before you size the round, set the dilution budget, because that is the half of the equation founders skip. Fred Wilson's rule is to dilute in the 10 to 20 percent band every time you raise, because, in his words, 'If you do two or three rounds at north of 20% each round, you'll end up with too little of the company.' YC's guide says 10 percent is wonderful, most rounds will require up to 20 percent, and you should try to avoid more than 25. Paul Graham draws the same ceiling: no more than 25 percent in the main raise, on top of less than 15 percent sold before it.

The market sits exactly where the advice says it should. Carta's State of Seed report for winter 2025 shows founders typically sell about 20 percent in a priced seed round, leaving the median founding team with 56.2 percent of fully diluted equity. Median Series A dilution on Carta was 17.9 percent in Q1 2025, down from 20.9 percent a year earlier. The pattern holds even before a priced round: Carta's SAFE data shows that raising $1 million to $1.9 million on SAFEs implies a median 15.6 percent of expected dilution, while $5 million to $5.9 million implies 23.7 percent.

And it compounds. Carta's founder ownership data shows the median founding team falling from about 56 percent at seed to about 36 percent by Series A. Wilson's lifetime math is harsher still: three to four rounds of equity plus the 20 to 25 percent it takes to recruit and retain a management team leaves founders of companies that go the distance with roughly 10 to 20 percent at exit, and he has seen founders finish below 5. A round costs 15 to 20 percent whether you raise $2 million or $6 million, so the raise divided by the budget is your implied valuation. That is the whole disguise.

The case against raising too much

Raising too little kills fast and obviously. Raising too much kills slowly, in three ways, and I see the results in valuation work all the time.

First, the bar. Graham's example is the cleanest: 'If you raise money in phase 2 at a post-money valuation of $30 million, the pre-money valuation of your next round is going to have to be at least $50 million', and only a company doing really, really well clears that. Every extra dollar raised inside a fixed dilution budget pushes the price up, and every dollar of price is a promise the next eighteen months must keep. In my experience, down rounds are rarely caused by bad companies. They are caused by decent companies that priced the last round for a better one.

Second, burn creep. Graham again: 'The more you raise, the more you spend, and spending a lot of money can be disastrous for an early stage startup.' Spending makes profitability harder and makes you rigid, because money is mostly spent on people and headcount is hard to reverse. His advice to the founder who raises a huge round anyway: don't spend it. Marc Andreessen said the same thing from the other side of the table in September 2014, warning publicly that burn rates were dangerously high and that when the market turned, high-burn companies would 'vaporize' because nobody funds or acquires a cash incinerator.

Third, the stack. In a standard structure, each preferred round adds its invested capital to the liquidation preference stack, so at a 1x preference the money sitting ahead of common stock at exit is, at minimum, everything you have ever raised. Scott Kupor's Secrets of Sand Hill Road walks through exactly how that stack gets paid before founders and employees see anything. Wilson adds the quieter cost of overraising: take much more than 18 months of cash and a fast-growing company spends year two 'sitting on cash that you raised when your company was worth considerably less'. That is cheap dilution, sold early, plus a preference sitting on top of it.

The case against raising too little

None of this makes underraising smart. It just makes the trade explicit.

Wilson's floor is as firm as his ceiling: less than a year of cash forces founders back into the market too quickly. And fundraising is not a weekend. The original DocSend study with Harvard Business School's Tom Eisenmann, covering 200 startups that raised over $360 million, found the average seed raise took contact with 58 investors, 40 meetings, and 12.5 weeks to close, for an average of $1.3 million. One fifth of successful rounds took 20 weeks or longer; the longest took 40. The market has since gotten less efficient, not more: DocSend's 2023 seed report found founders contacting 66 investors on average, up from 48 in 2022, while getting only 38 meetings, down from 56, and half of successful raises took 13 to 24 weeks. That is a quarter to half a year of founder attention, and it comes straight out of the product. The same research holds a warning for the spray-and-pray instinct: contacting more investors did not correlate with raising more money.

The other cost of underraising shows up in Carta's bridge data. In Q1 2024, 42 percent of seed rounds and 43 percent of Series A rounds on Carta were bridge rounds, decade highs. Meanwhile Carta's State of Seed shows the median time from seed to Series A has stretched to 2.1 years, up from 1.5 in 2019, and only about half of seed-funded companies reach an A within four years. If you sized your runway for the 2019 market, the gap between 1.5 years and 2.1 is a bridge round with your name on it. And bridges get raised at your weakest moment, from your existing investors, on their terms.

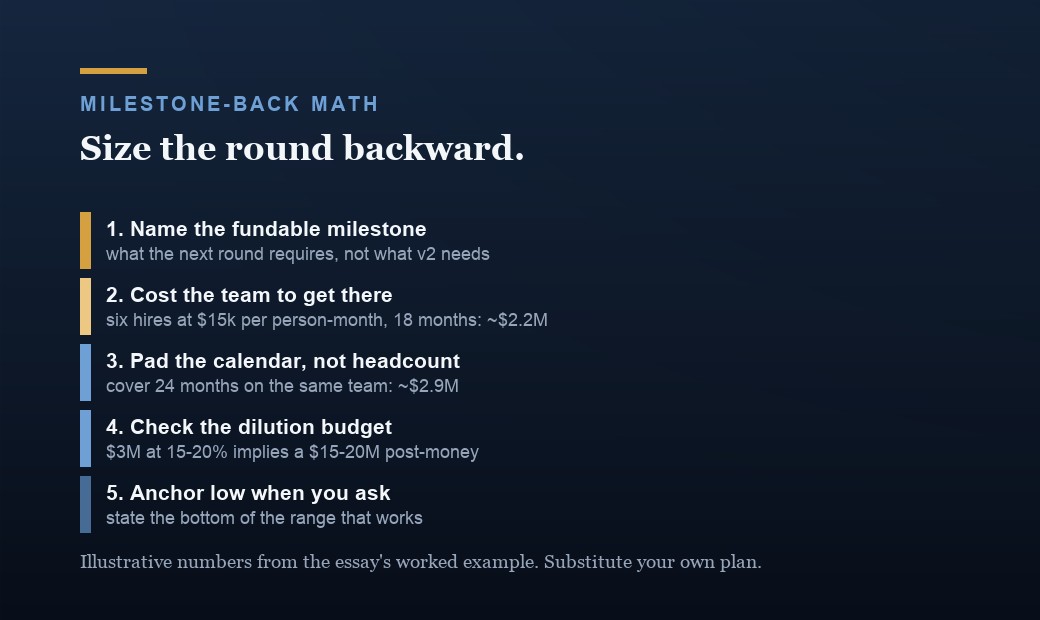

How to size it: milestone-back math

Here is the sequence I would run, with a worked example. Every number in the example is illustrative, not a benchmark. Substitute your own.

Step one, name the milestone. Not 'launch v2'. A fundable milestone: the state of the business at which the next round clears. For SaaS, Jason Lemkin's published Series A benchmarks are as good a target as any: most companies raising an A are doing $1 million to $2.5 million in ARR, growing 7 to 15 percent month over month into the raise, with CAC payback ideally under 12 months and a credible case for tripling revenue within a year. Suppose you are at $250,000 ARR after a pre-seed. Your milestone is, say, $1.5 million ARR with that growth shape intact.

Step two, cost the team that gets you there. Suppose that takes six hires beyond the founders: four engineers, two go-to-market. On the Graham and YC number of $15,000 per person per month all-in, six people for 18 months is $1.62 million. Add two founders on modest salaries plus fixed costs and call the 18-month plan roughly $2.2 million.

Step three, pad the calendar, not the headcount. The seed-to-A median is now 2.1 years on Carta, so cover 24 months on the same team: roughly $2.9 million. Call the ask $3 million. The padding buys time, not people. This is where the extra months of the two-year fashion legitimately come from.

Step four, check the dilution budget. $3 million at 15 to 20 percent implies a $15 million to $20 million post-money. Carta's market medians say that is a coherent ask: the median seed in the winter 2025 State of Seed was $4 million at a $20 million post, and the median seed pre-money on Carta was $16 million in Q1 2025. Now run the counterfactual: taking $6 million 'because it was offered' at the same budget claims a $30 million post, and Graham's next-round bar starts to loom over a company that has not earned it yet.

Step five, anchor low when you ask. Graham's tactic: state a number at the bottom of the range that works, because 'There is almost no downside in starting with a low number. It not only won't cap the amount you raise, but will on the whole tend to increase it.' You can always raise the target. You cannot un-anchor a number you failed to hit.

The mistakes that cost the most

After a thousand-plus valuations, the expensive mistakes repeat.

Sizing to the press release. Your competitor's $8 million round tells you nothing about your milestone or your dilution budget. Medians are more honest than trophies: Carta's median seed is $4 million cash while the 95th percentile is $16.6 million, and the PitchBook-NVCA Venture Monitor for Q1 2026 puts the median US seed at $3 million and the median Series A at $19.6 million. Different data sets, same lesson. The rounds you remember from headlines are the outliers.

Not knowing whether you are default alive. Graham reports that 'Half the founders I talk to don't know whether they're default alive or default dead': whether, at current expenses and growth, the company reaches profitability on the money it has. He says to start asking within the first 8 or 9 months, because the alternative is what he calls the fatal pinch: unprofitable, growing slowly, and without enough runway left to fix either.

Hiring into the raise. Graham calls overhiring by far the biggest killer of startups that raise money, and notes that the large staffs of successful startups are probably more the effect of growth than the cause. The raise is fuel for a working engine, not the parts list for building one.

Planning the raise as a six-week sprint. In the DocSend data, companies that failed to raise gave up after 6.7 weeks on average, right around the point where the successful ones were halfway through a 12.5-week average process. Founders in that study rated the length 3.6 on a 5-point scale where 3 meant 'as expected'. It always takes longer than the plan.

Assuming the follow-on. Graham's discipline is the one I would staple to every term sheet: know, as in write down, precisely what you will need to do to survive if you cannot raise more money. Size this round as if it were the last one, because in Carta's data, for about half of seed companies, it effectively is.

The takeaway

The right raise is the smallest number that credibly buys your next fundable milestone, padded for the market's real timeline rather than the 2019 one, inside a 15 to 20 percent dilution budget, at an implied price you can step up from without a miracle. Run the milestone math, check it against the medians, anchor low, and keep the plan alive that assumes no one ever funds you again.

That number will usually sound less impressive than what your competitor announced and less flattering than what an eager investor is offering. Take it anyway. A round is not a scoreboard and it is not validation. It is a forward sale of a piece of your company at a price you will be asked to justify, by someone like me, roughly eighteen months from now. The ask is the valuation. Size it like one.

Common questions

How many months of runway should a startup raise?

The canonical sources converge on 12 to 18 months. Y Combinator's seed guide says to raise enough to reach your next fundable milestone, usually 12 to 18 months out; Fred Wilson calls 12 to 18 months of cash ideal for seed through Series B; Paul Graham's sizing formula uses 18 months. But the market has slowed since that advice was written: the median time from seed to Series A on Carta is now 2.1 years, up from 1.5 in 2019. Padding toward 24 months is sensible current practice, provided you pad the calendar, not the headcount.

What percentage of my company should I sell in a seed round?

Aim for 10 to 20 percent and treat 25 as a hard ceiling. Fred Wilson's rule is to dilute in the 10 to 20 percent band every round; YC's guide says most seed rounds require up to 20 percent and more than 25 should be avoided; Paul Graham sets the same 25 percent limit. The market lands right there: Carta data shows founders typically sell about 20 percent in a priced seed, leaving the median founding team with 56.2 percent, which falls to roughly 36 percent by Series A. Dilution compounds, so budget it across rounds, not per round.

Is it bad to raise more money than you need?

It carries three real costs. It raises the bar: Paul Graham points out that a $30 million post-money round means the next round has to price at $50 million pre or better. It fuels burn creep: the more you raise, the more you spend, mostly on people, and Graham identifies overhiring as by far the biggest killer of startups that raise money. And at a standard 1x liquidation preference, every dollar raised sits ahead of common stock at exit. If you do take a big round anyway, Graham's rule applies: don't spend it.

How long does a seed round take to raise?

Longer than most founders plan for. The original DocSend study with Tom Eisenmann found the average seed raise involved contacting 58 investors, holding 40 meetings, and taking 12.5 weeks to close, with one fifth of successful rounds taking 20 weeks or more. By 2023, DocSend found founders contacting 66 investors for only 38 meetings, and half of successful raises took 13 to 24 weeks. The telling number: companies that failed to raise gave up after 6.7 weeks on average. Budget four to six months of calendar and keep running the business while you raise.

What metrics do I need to raise a Series A?

Jason Lemkin's SaaStr benchmarks: most SaaS companies raising a Series A are doing $1 million to $2.5 million in ARR, growing 7 to 15 percent month over month into the raise, with CAC payback ideally under 12 months and a credible case for tripling revenue within a year. Typical rounds run $5 million to $15 million. On pricing, Carta's Q1 2025 median Series A pre-money was $48 million, with median dilution of 17.9 percent. And respect the base rate: only about half of seed-funded companies reach a Series A within four years.

Related reading

- How VCs actually decide whether to fund you.

- Raising on SAFEs: the dilution you signed and forgot.

- How to value a pre-revenue startup, from someone who prices them.

- How to handle a down round when the terms matter more than the price.

Go deeper

If you are sizing a round right now, let's work through the milestone plan, the dilution budget, and the implied valuation together before you start the roadshow, or read more of how I think about it.

Tomasz Felpel is an investor, founder, and advisor in private markets and healthcare, based in New York. He is a three-time founder of Value Alpha, an AI-powered private-markets valuation platform, Sonnerie VC, an early-stage healthcare venture firm, and Pond. Previously he led corporate development and M&A at Fortune 500 scale, pricing more than 1,000 private companies. Columbia Business School EMBA. Read the full story.