Founders · Fundraising

How VCs actually decide whether to fund you

The partner in the room is not the decision. A funnel, a portfolio model, and an ownership target are. Here is the machine, with real numbers, from someone who sits on both sides of the table.

You are pitching a machine, not a person

I price private companies for a living. I have priced more than a thousand of them, on deals up to roughly $26 billion, and I write early-stage checks through my own fund. That puts me on both sides of the table, and from the investor side I watch founders make the same mistake every single week: they pitch the meeting in front of them as if the person in the room were the decision. The person is not the decision. The person is a component in a machine, and the machine is running a funnel, a portfolio model, and an ownership target you will never see.

When the partner says this is really interesting, let's stay in touch, you hear a maybe from a human. What actually happened is that you were routed to a stage in a process that had conversion rates before you walked in. Every question you got, about market size, about your co-founder, about round size, was the machine checking you against a model. Founders who do not know the machine exists optimize the wrong stage of it. So here is the machine, with the real numbers attached.

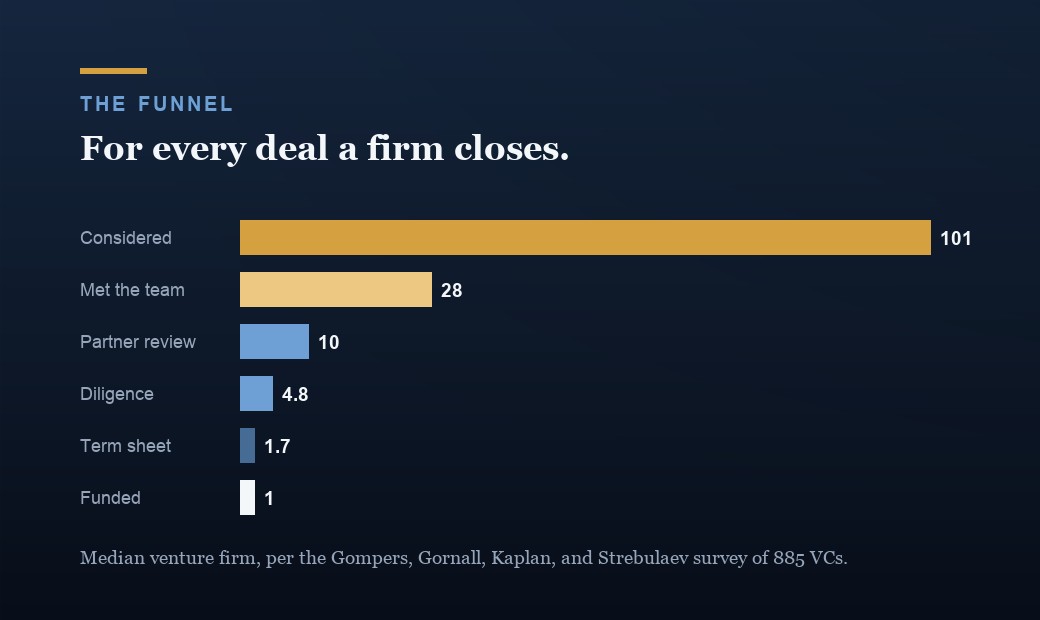

The funnel and its real numbers

The best public map of the machine is the study by Gompers, Gornall, Kaplan, and Strebulaev, published in the Journal of Financial Economics in 2020, a survey of 885 institutional venture capitalists at 681 firms. One caveat: it was fielded in 2015 and 2016 and the numbers are self-reported. Treat them as the shape of the machine, not its serial number.

Here is the shape. For each deal a firm closes, it considers on average 101 opportunities. Of those 101, 28 get a meeting with management, 10 get reviewed at a partners meeting, 4.8 go into due diligence, 1.7 receive a term sheet, and one closes. The median firm's year looks the same: 200 investments considered, 50 management meetings, 20 partner reviews, diligence on 12, 5.5 term sheets, about 4 deals closed. Four. The firm you are pitching says yes roughly four times a year.

Two details in that table matter more than founders realize. First, sector changes the funnel: an IT-focused firm considers 151 deals per investment while a healthcare firm considers only 78, which the authors attribute to the higher fixed cost of evaluating healthcare deals and the smaller universe of healthcare founders. Your odds depend on which aisle you are standing in. Second, firms offer 1.7 term sheets per closed deal, a close rate of roughly 60 percent, which the authors say suggests many funded deals are not proprietary. Translation: VCs lose deals they wanted. Competition between term sheets is real, and I will show you how to manufacture it.

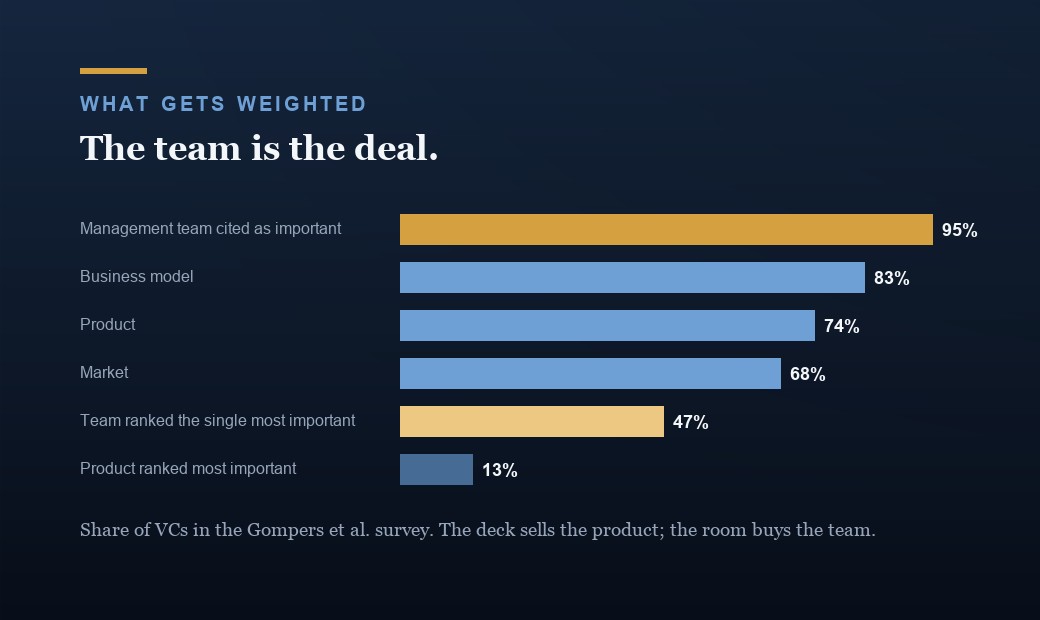

What actually gets weighted

The same study asked what drives selection. The management team was cited as important by 95 percent of firms and as the single most important factor by 47 percent. Business model came in at 83 percent, product at 74 percent, market at 68 percent, industry at 31 percent. All the business factors combined, what the authors call the horse, were rated most important by only 37 percent of firms. The jockey wins the survey.

VCs are specific about what team means. Ability was the most-mentioned trait, cited by more than two thirds of respondents, followed by industry experience, then passion, entrepreneurial experience, and teamwork. Asked what drove outcomes after investment, they credited the team in 96 percent of successes and blamed it in 92 percent of failures, while industry, business model, technology, and timing each showed up in only 45 to 58 percent of failures. In a detail I find genuinely funny, they did not cite their own contributions in either direction. Self-reported data always has a hero, and it is never the narrator.

The practical consequence: your team slide is the product being purchased. Lead with evidence of ability, things shipped, speed between milestones, hard problems solved, then specific industry experience. Most founders spend 80 percent of the pitch on the horse when nearly half the buyers walked in to evaluate the jockey.

Where deals actually come from

Now look at how deals enter the funnel at all, because this is where cold outreach gets hurt. In the Gompers study, more than 30 percent of deals came through the VCs' professional networks, 20 percent were referred by other investors, 8 percent came from existing portfolio companies, and almost 30 percent were proactively self-generated by the firm. Inbound from company management, the cold email, was 10 percent. Nine out of ten deals a firm even considers arrive through a channel you were not using.

I built my career without a network, so I will not romanticize warm intros. But the referred path is the wide path, and the smart move is to engineer the referral rather than send the hundredth cold deck. A portfolio founder is an 8 percent channel by himself. An investor who passed but liked you is a 20 percent channel. And the 30 percent self-generated share is the outsider's loophole: firms actively hunt, so publishing your metrics, your thesis, your build in public turns their outbound into your inbound. Cold email is not dead. It is just the narrowest door into the building.

The three minutes your deck actually gets

You wrote the deck over six weeks. Here is how long it gets read. In a DocSend study run with Harvard Business School professor Tom Eisenmann, covering more than 200 startups that raised a combined $360 million, investors spent an average of 3 minutes 44 seconds per pitch deck. That was 2015. DocSend's platform-wide data has the number falling ever since, hitting an all-time low of 2 minutes 24 seconds in the fourth quarter of 2023. Different methodologies, same direction. The deck is a screening artifact, not a persuasion artifact. Its only job is to buy the meeting.

The same 2015 study measured which slides investors studied longest: financials, team, and competition. Not vision. Not product screenshots. The three slides founders most often rush are the three slides investors slow down on. Even pre-revenue, show a real financial model, name your competitors honestly, and put the team evidence early. A deck that survives three minutes of skeptical scrolling is a deck built around those three slides.

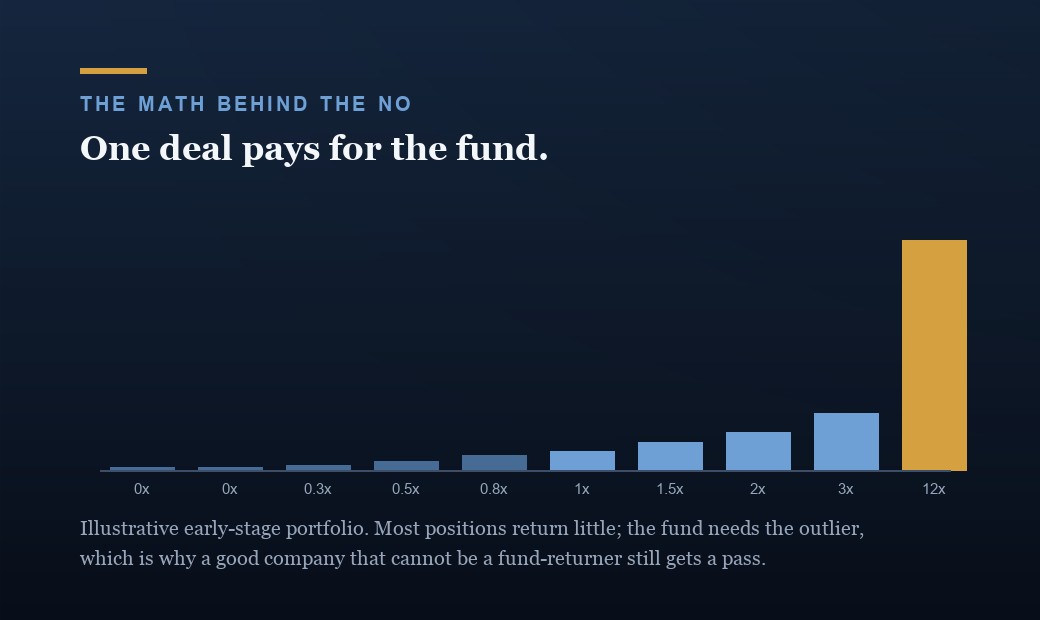

The portfolio math behind the no

To understand why the funnel is so brutal, you need the return math underneath it. Correlation Ventures analyzed more than 21,000 venture financings from 2004 to 2013: 65 percent failed to return even 1x capital, only 10 percent returned 5x or more, and only 4 percent returned 10x or more. Horsley Bridge portfolio data, published by Chris Dixon at a16z, shows about 6 percent of investments generated about 60 percent of total returns, with home runs in the best funds averaging around 70x versus around 20x in merely good funds. Paul Graham wrote in 2012 that two companies, Dropbox and Airbnb, accounted for about three quarters of the roughly $10 billion in total value Y Combinator had funded. Venture returns are not a bell curve. They are a lottery with a visible ticket structure.

So every fund is built backwards from the outliers. Fred Wilson has described USV's model publicly: 20 to 25 investments per fund, an expectation that 2 or 3 become high-impact companies that can each return the entire fund, ownership of 15 to 20 percent in those companies defended round after round, and exits at a billion dollars or more. When a partner looks at you, the question is not whether this is a good business. The question is whether this can be one of the two or three. A likely 3x is a polite no in a model that needs a possible 70x.

And here is the part I can confirm from pricing companies every day: the valuation you are offered is often not an opinion about your company at all. In the Gompers study, roughly half of VCs set valuation mechanically from the investment amount and their target ownership percentage, early-stage investors most of all. Exit considerations ranked as the most important valuation factor, comparables second, desired ownership third; competitive pressure was rated most important by only 3 percent. Formal finance is barely in the room: only 22 percent of VCs use DCF, 9 percent use no quantitative metric at all, and 20 percent do not even forecast your cash flows. Where return targets exist, the averages are a 31 percent IRR and a 5.5x multiple. Your valuation is frequently their check size divided by 20 percent. I say this as someone whose day job is valuation: at the early stage, the machine prices ownership, not enterprise value.

What kills deals in diligence

Say you make it to diligence, one of the 4.8. The Gompers study puts the average deal at 83 days from start to close, with 118 hours of due diligence and 10 reference calls, 8 at early-stage firms and 13 at late-stage. That is a quarter of a year of someone actively looking for a reason to say no. And a term sheet is not the finish line: firms offer 1.7 for every close, so signed paper still fails roughly 40 percent of the time.

What actually kills deals, from my seat on both sides: first, the references. VCs attribute 92 percent of failures to the team, per Gompers, so those 10 calls are the real diligence, and one hesitant former colleague outweighs a quarter of great metrics. Second, numbers that do not reconcile. When the data room tells a slightly different story than the deck did, the problem stops being the numbers and becomes you. Third, the cap table, the killer founders least expect.

Y Combinator's seed fundraising guide is blunt: giving up 10 percent is wonderful, most rounds require up to 20 percent, avoid more than 25. Per Carta data, median dilution at seed and Series A has clustered around 19 to 20 percent for years; a 2023 dataset of 1,229 US priced rounds put median seed dilution at 20.5 percent. Investors check your cap table against those norms because of the fund math above: sell 45 percent before the A and the next investor cannot take their 15 to 20 percent without crushing the founder motivation the model treats as the core asset. A broken cap table does not get negotiated. It gets passed on.

How to run your raise against the machine

Once you accept that you are pitching a process with conversion rates, the playbook writes itself. First, size the effort honestly. The DocSend and Eisenmann study found companies needed an average of 40 investor meetings and a little over 12 weeks to close a round, with Series A rounds averaging 9.6 weeks and founders contacting an average of 26 investors. It also found no correlation between the number of meetings and the amount raised, so this is not a volume game, it is a parallel game. Start every conversation in the same window so term sheets land near each other. The 60 percent term-sheet close rate exists because firms compete. Make them.

Second, qualify the firm before you pitch: stage, sector, fund size against your round, and how much of the fund is left to deploy, because the median firm closes about four deals a year and a firm at the end of its fund says no to everything, politely. Third, protect the cap table. Budget roughly 20 percent dilution, in line with the Carta norms, and walk away from structures that quietly take more. Fourth, raise for the bar that actually exists. Per Carta cohort data, 30.6 percent of Q1 2018 seed companies reached a Series A within two years; for the Q1 2022 cohort it was roughly 15.4 percent. The graduation rate halved. Size the round to hit Series A metrics, not to shave dilution to the decimal.

The takeaway

The machine is not cruel. It is arithmetic. When 65 percent of financings lose money, per Correlation Ventures, and 6 percent of investments produce 60 percent of returns in the Horsley Bridge data, a rational investor builds a funnel that says no a hundred times per yes and a portfolio that only needs two winners. None of it is a verdict on you.

So stop pitching the person and start fitting the model. Enter through a referral, lead with the jockey, build the deck around the three slides that get read, keep the cap table inside the norms, and run the process in parallel until the machine produces its own competition. The partner across the table would usually love to say yes. Your job is to make the machine let them.

Common questions

How many investors do I need to pitch to raise a round?

Plan for dozens, not a handful. The DocSend study with HBS professor Tom Eisenmann found companies averaged 40 investor meetings and a little over 12 weeks to close a round, and founders contacted an average of 26 investors for a Series A, and 58 at seed. On the firm side, Gompers and coauthors found VCs consider 101 opportunities and meet 28 management teams for every deal they close. A single pass carries almost no information, because the base rate is passing. Build a qualified list of 30 to 50 firms, run the conversations in parallel, and treat the raise as a full-time job for one founder for a quarter.

Do VCs care more about the team or the market?

Team, and it is not close. In the Journal of Financial Economics survey of 885 VCs by Gompers, Gornall, Kaplan, and Strebulaev, 95 percent rated the founding team important and 47 percent rated it the single most important factor, versus 37 percent for all business factors combined. Within team, ability was the most-cited trait, ahead of industry experience and passion. The same VCs attributed 96 percent of their successes and 92 percent of their failures to the team. Put the team evidence early in the deck and expect the reference calls to decide the deal.

Is cold emailing VCs a waste of time?

Not a waste, but it is the narrowest channel. Per the Gompers study, only 10 percent of deals VCs consider come inbound from company management, while over 30 percent arrive through the firm's professional network, 20 percent from other investors, and 8 percent from portfolio companies. Almost 30 percent are self-generated by the firm, which is the outsider's loophole: firms hunt, so make yourself findable through published metrics, a public thesis, and visible shipping. The highest-yield move is converting a cold contact into a warm one by getting a portfolio founder or an angel to forward you.

How long does it take a VC to close a deal?

The average deal takes 83 days from start to close, per Gompers and coauthors, and over that window the average firm spends 118 hours on due diligence and calls 10 references, 8 at early-stage firms and 13 at late-stage ones. A term sheet is not the finish line either: firms offer 1.7 term sheets for every deal that closes, a close rate of roughly 60 percent. Budget a full quarter from first partner meeting to money in the bank, and keep at least one competing conversation alive until the wire clears.

How much of my company should I sell in a seed round?

The norms are tight. Y Combinator's seed guide says giving up 10 percent is wonderful, up to 20 percent is typical for most rounds, and more than 25 percent should be avoided. Carta's cap table data shows median dilution at seed and Series A clustered around 19 to 20 percent, with a 2023 dataset of 1,229 US priced rounds putting median seed dilution at 20.5 percent. Investors check against those numbers because their fund model, like USV's stated 15 to 20 percent ownership target, needs room in future rounds. Sell much more than a quarter and you become the diligence problem.

Related reading

- Raising on SAFEs: the dilution you signed and forgot.

- How to value a pre-revenue startup, from someone who prices them.

- How to know you have product-market fit, read like an investor.

- How to handle a down round when the terms matter more than the price.

Go deeper

If you are heading into a raise, let's pressure-test the pitch and the raise plan against how the machine actually reads them, the deck, the cap table, the target list, and the sequencing, before the first partner meeting, or read more of how I think about it.

Tomasz Felpel is an investor, founder, and advisor in private markets and healthcare, based in New York. He is a three-time founder of Value Alpha, an AI-powered private-markets valuation platform, Sonnerie VC, an early-stage healthcare venture firm, and Pond. Previously he led corporate development and M&A at Fortune 500 scale, pricing more than 1,000 private companies. Columbia Business School EMBA. Read the full story.